404

+1-313-307-4176

Automotive Smart Display Market Analysis | 2024-2032

Automotive Smart Display Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2024-2032

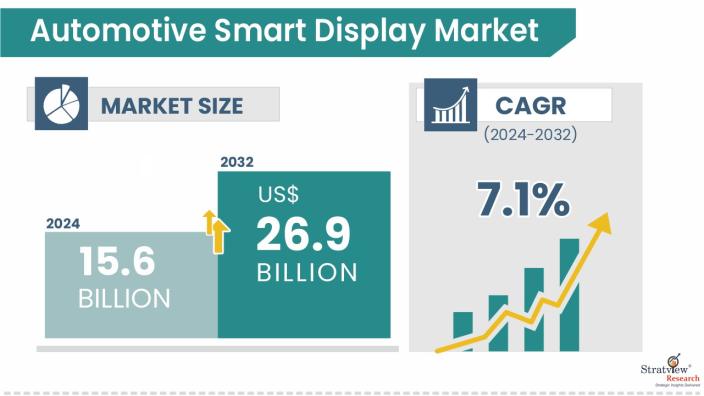

The automotive smart display market size was USD 15.6 billion in 2024 and is likely to grow at a CAGR of 7.1% during 2024-2032 to reach USD 26.9 billion in 2032.

Want to know more about the market scope? Register Here

The automotive smart display Market refers to the segment of the automotive technology industry that focuses on the development and integration of advanced display systems within vehicles. These smart displays serve as crucial interfaces for both drivers and passengers, providing real-time information, entertainment, navigation, and enhanced vehicle control. This market encompasses a wide range of technologies and solutions, including touchscreens, heads-up displays (HUDs), digital instrument clusters, and augmented reality displays. With the growing demand for connected cars, autonomous driving features, and improved user experience, the automotive smart display market plays a vital role in enhancing vehicle safety, comfort, and functionality while enabling seamless interaction between the driver, vehicle, and external environment.

In the automotive smart display market, companies are increasingly forming strategic alliances, including mergers, acquisitions, and joint ventures, to drive innovation and expand their technological capabilities. This trend is fueled by the rising demand for connected vehicles, enhanced infotainment systems, and digital cockpits that offer improved user interaction and real-time vehicle information. Automotive manufacturers and technology providers are collaborating to merge expertise in hardware design, software development, and system integration, enabling the development of smart displays that support seamless connectivity, intuitive interfaces, and advanced driver assistance features.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Application-Type Analysis |

Center Stack, Digital Instrument Cluster, Head-up Display, Rear Seat Entertainment |

Center Stack is projected to be the largest segment due to its role as a multifunctional infotainment hub. Its integration with telematics, navigation, and climate controls, along with demand for user-friendly interfaces in connected and semi-autonomous vehicles, is driving strong adoption across regions. |

|

Display Size Type Analysis

|

<5”, 5”-10”, >10” |

>10” Displays are expected to experience strong growth due to increasing integration in semi-autonomous and high-end vehicles for enhanced visualization, improved ADAS integration, and better in-vehicle communication. |

|

Display Technology-Type Analysis |

LCD, TFT-LCD, OLED, Others |

OLED Displays are gaining traction for their superior image quality, flexibility, and thin form factor. As OEMs demand more immersive and visually appealing displays in luxury and mid-range vehicles, OLED is expected to see high growth. |

|

Autonomous Driving-Type Analysis |

Semi-autonomous, Autonomous |

Semi-Autonomous Vehicles are expected to dominate the market. Increasing electrification, consumer demand for safety and driver-assist features, and OEM investment in ADAS technologies are driving smart display adoption. Center stack and HUD displays are key interfaces enabling safer, more interactive driving experiences. |

|

Electric Vehicle-Type Analysis |

BEV, FCEV, HEV, PHEV. |

Battery Electric Vehicles (BEV) are expected to contribute significantly to smart display growth, given their dependence on digital interfaces for range, charging, and system monitoring. As EV adoption increases globally, demand for intelligent and adaptive display solutions will rise. |

|

Vehicle Class-Type Analysis |

Economy, Mid-Segment, Luxury |

Mid-Segment Vehicles are expected to dominate the market during the forecast period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

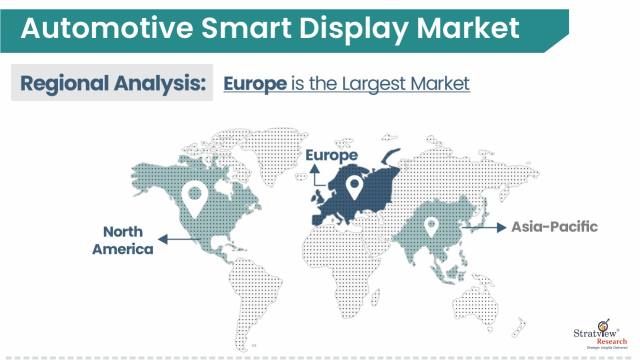

Europe is expected to be the largest market for the Automotive Smart Display Market |

“Center Stack is expected to dominate the automotive smart display market during the forecast period.”

Based on application, the market is segmented into Center Stack, Digital Instrument Cluster, Head-up Display, and Rear Seat Entertainment. The Center Stack segment is projected to lead the market due to its increasing integration as a multifunctional control and infotainment interface in modern vehicles. With features such as navigation, music, HVAC controls, and smartphone connectivity, center stacks have become essential for enhancing the in-car user experience. The rise of connected, semi-autonomous, and electric vehicles is further accelerating demand for advanced center stack displays.

“>10” Display segment is expected to dominate during the forecast period.”

Based on display size, the market is categorized into <5”, 5”–10”, and >10”. The >10” segment is anticipated to grow the fastest due to increased demand for larger displays that support multi-functionality and higher resolution. Luxury and electric vehicles are leading adopters of widescreen infotainment displays, while larger screen real estate also enables better integration with driver-assist technologies and entertainment features, especially in semi-autonomous vehicles.

“OLED is expected to be the fastest-growing display technology in the market.”

The display technology segment includes LCD, TFT-LCD, OLED, and Others. Among these, OLED is expected to experience rapid growth due to its superior image clarity, energy efficiency, flexible form factor, and thin profile. These characteristics make OLEDs ideal for futuristic cockpit designs and curved dashboard displays, especially in premium and electric vehicles.

“The Semi-Autonomous Vehicles segment is expected to dominate the market.”

Based on the level of autonomy, the market is segmented into Semi-Autonomous and Autonomous. Semi-Autonomous Vehicles are expected to dominate due to the growing integration of ADAS features, driver monitoring systems, and interactive smart displays that assist in driving. OEMs are investing heavily in this segment to balance advanced functionality with driver control, making it the leading use case for smart display technology.

“Battery Electric Vehicles (BEVs) are expected to lead the smart display market.”

Segmented into BEV, HEV, PHEV, and FCEV, the BEV category is expected to be the most influential. BEVs rely heavily on digital dashboards and infotainment systems for essential functions like battery monitoring, energy usage, and real-time navigation. As governments push for cleaner mobility and OEMs expand their electric portfolios, BEVs are emerging as primary consumers of advanced smart displays that enhance usability and connectivity.

“Mid-Segment vehicles are expected to drive market growth.”

The market is segmented by vehicle class into Economy, Mid-Segment, and Luxury. Mid-Segment vehicles are anticipated to lead in smart display adoption as they incorporate high-end features such as digital cockpits, head-up displays, and AR-enabled interfaces. These vehicles often act as test beds for emerging display technologies and offer consumers a premium user experience, driving strong demand.

“Passenger Cars are expected to dominate the market, followed by growth in Light and Heavy Commercial Vehicles.”

The market is segmented by vehicle type into Passenger Cars, Light Commercial Vehicles (LCVs), and Heavy Commercial Vehicles (HCVs). Passenger cars are anticipated to continue as the dominant segment for smart display adoption, driven by increasing consumer demand for advanced infotainment systems, connected technologies, and driver-assistance features.

“Europe is projected to dominate the market, followed by strong growth in Asia Pacific and North America.”

The market is segmented by region into North America, Europe, Asia Pacific, and Rest of the World (RoW). Europe is expected to hold the largest market share for automotive smart displays, driven by technological advancements, strong adoption of connected and electric vehicles, and the presence of premium vehicle manufacturers.

Know the high-growth countries in this report. Register Here

The market is moderately fragmented. Most of the major players adopted partnerships, new product launches and jointy ventures to gain in automotive smart display market The following are the key players in the Automotive Smart Display Market . Some of the major players provide a complete range of services.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The automotive smart display market is segmented into the following categories.

By Application Type

By Display Size Type

By Application Type

By Autonomous Driving Type

By Electric Vehicle Type

By Vehicle Class Type

By Vehicle Class Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The automotive smart display market refers to the industry focused on the development, production, and integration of advanced digital screens and interactive display technologies within vehicles. These displays are designed to enhance the driver and passenger experience by providing critical vehicle information, entertainment, connectivity, and safety features in a visually rich and user-friendly format.

The forecasted value for the market is expected to be USD 26.9 billion in 2032.

The automotive smart display market is likely to grow at a CAGR of 7.1% during 2024-2032.

Key factors that are driving the market are as follows: • Rising demand for in-car connectivity and infotainment systems • Shift toward electric and autonomous vehicles • Technological advancements in display technology (OLED, QLED, etc.). • Growing adoption of Advanced Driver Assistance Systems (ADAS).

One standout growth opportunity in the automotive smart display market is the rising adoption of Head-Up Displays (HUDs). Originally limited to premium vehicles, HUDs are now being increasingly integrated into mid-range models as costs decrease and safety standards rise. These displays project critical driving information—like speed, navigation, and ADAS alerts—directly onto the windshield, allowing drivers to stay informed without taking their eyes off the road.

Asia-Pacific currently holds the largest share of the global automotive smart display market. This leadership is driven by the high volume of vehicle production, strong demand for connected and electric vehicles, and rapid technological adoption in countries like China, Japan, and South Korea. China, in particular, is a major contributor due to its booming automotive sector and growing consumer preference for in-car technology.

The key players in the automotive smart display market include Bosch, Continental, Denso, Visteon, Nippon Seiki, Panasonic, Pioneer, and Yazaki.

WE ACCEPT