404

+1-313-307-4176

Hydrogen Catalyst Layer Market Analysis | 2025-2035

Hydrogen Catalyst Layer Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2025-2035

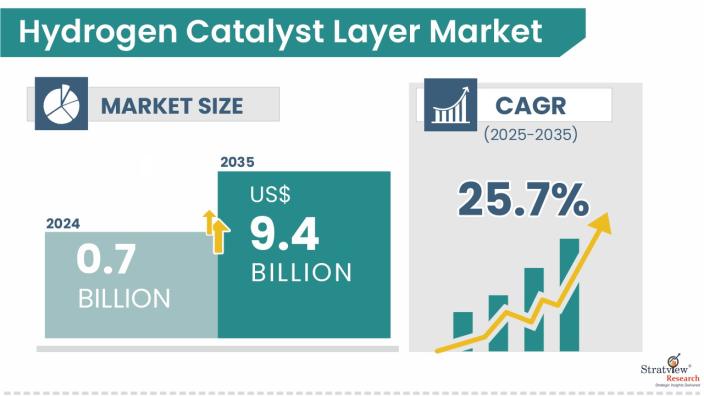

"Hydrogen catalyst layer market size was USD 0.7 billion in 2024.”

The market is expected to reach USD 1.0 billion in 2025, witnessing an annual growth of 28.3%.

The market size will reach USD 9.4 billion in 2035, witnessing a market growth (CAGR) of 25.7% during the forecast period of 2025-2035.

The annual demand for hydrogen catalyst layer was USD 0.7 billion in 2024 and is expected to reach USD 1.0 billion in 2025, up 28.3% than the value in 2024.

During the forecast period (2025-2035), the hydrogen catalyst layer market is expected to grow at a CAGR of 25.7%. The annual demand will reach USD 9.4 billion in 2035, which is almost 9 times the demand in 2025.

During 2025-2035, the hydrogen catalyst layer industry is expected to generate a cumulative sales opportunity of USD 47.6 billion, which is almost 11 times the opportunities during 2019-2024.

Wish to get a free sample? Click Here

Asia-Pacific generated the highest demand with the largest market share of more than 55% in 2024.

By stack system type, Fuel Cells have been the leading stack system employing the catalyst layer and will maintain their lead in the forecast period.

By base material type, Platinum-based materials have dominated the market in the past and will continue to reign in the forecast period

Have a look at the sales opportunities presented by the hydrogen catalyst layer market in terms of growth and market forecast.

|

Hydrogen Catalyst Layer Market Data & Statistics |

|

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

|

Annual Market Size in 2024 |

USD 0.7 billion |

- |

|

|

Annual Market Size in 2025 |

USD 1.0 billion |

YoY Growth in 2025: 28.7% |

|

|

Annual Market Size in 2035 |

USD 9.4 billion |

CAGR 2025-2035: 25.7% |

|

|

Cumulative Sales Opportunity during 2025-2035 |

USD 47.6 billion |

- |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 0.6 billion + |

> 80% |

|

|

Top 10 Company’s Market Share in 2024 |

USD 0.3 billion to USD 0.5 billion |

50% - 70% |

|

What is the hydrogen catalyst layer?

The catalyst layer (electrode and catalyst material) is a fundamental building block of fuel cells and electrolyzers and the heart of the Membrane Electrode Assembly (MEA), in which the most important electrochemical reactions occur. Located between the membrane and the gas diffusion layer, it makes the principal reactions possible: hydrogen oxidation and oxygen reduction in fuel cells and water splitting in electrolyzers. The catalyst facilitates these reactions by lowering the activation energy, while the electrode serves as the conducting surface for electron transfer. The layer directly influences efficiency, durability, and overall system performance. High-performance catalysts, typically made from platinum, iridium, or nickel alloys, play a central role in guaranteeing optimized energy conversion and stable operation under harsh conditions. Further, catalyst material dispersion and structure influence reaction kinetics, gas diffusion, and ion transport, and as such, optimization of this layer is necessary to minimize energy loss, enhance hydrogen and oxygen production rates to the maximum level, and enable cost-efficient and scalable clean energy technologies.

The hydrogen catalyst layer market is being driven by the explosive expansion of the hydrogen economy, particularly in fuel cells and electrolyzers for clean energy applications. Growing global demand for low-emission energy technologies, driven by climate goals and net-zero initiatives, is driving the use of fuel cells in the mobility and stationary power segments.

Concurrently, increasing demand for green hydrogen production is driving PEM electrolyzer adoption, thus instantaneously boosting demand for high-performance catalyst layers.

Policy support, government incentives, and increasing investments in hydrogen infrastructure also drive market growth. In addition, catalyst material breakthroughs, such as reduced platinum-group metal loading and catalyst dispersion enhancement are also boosting efficiency at lower expense, making the systems more economically viable.

The trend toward clean technologies, as well as mounting industrial and mobility applications, will significantly enhance the market for the catalyst layer. Growing demands for improved durability and performance are also pushing constant developments in the design and manufacturing of the catalyst layer.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Stack System-Type Analysis |

Fuel Cell and Electrolyzer |

Fuel Cells have been the leading stack system employing the catalyst layer and will maintain their lead in the forecast period. |

|

Base Material-Type Analysis |

Platinum-based, Palladium-based, Non-precious Metal Catalysts, and Other Base Materials |

Platinum-based materials have dominated the market in the past and will continue to reign in the forecast period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

The Asia-Pacific region is expected to maintain its reign over the forecast period. |

“Fuel cells have long been the dominant stack system utilizing catalyst layers and are set to retain their leading position well into the forecast period, driven by their proven performance, efficiency, and growing demand for clean energy solutions.”

Fuel cells have historically been the prevailing end-use of hydrogen catalyst layers and are expected to remain the leader throughout the forecast period based on their critical role in efficient and clean power generation.

The catalyst layer in fuel cells facilitates central reactions that convert hydrogen into electricity at high energy efficiency and minimal emissions. They are thus most appropriately applied in transportation, stationary power, and portable energy systems.

With more global attention on zero-emission mobility, countries like Japan, South Korea, and China are investing heavily in fuel cell electric vehicles (FCEVs) and hydrogen refueling stations.

As adoption rises, so does the demand for high-performance catalyst layers. Commercial readiness of fuel cell technology and its expanding commercial use ensure it is the main growth driver in the hydrogen catalyst layer market.

“Platinum-based materials have long dominated the market and are set to retain their leading edge well into the forecast period, due to their proven performance and reliability.”

The market is segmented into platinum-based, palladium-based, non-precious metal catalysts, and other base materials. Platinum-based materials have long held the hydrogen catalyst layer market and will continue to hold their leadership position well into the forecast period because of their excellent performance, reliability, and special electrochemical properties.

Platinum is most in demand because it has high mechanical strength, high conductivity, long lifespan, and high catalytic activity with rapid reaction kinetics. All these properties are especially essential in Proton Exchange Membrane (PEM) electrolyzers, where platinum is of most importance in optimizing the reaction rates with minimum wastage of energy to ensure maximum efficiency. Its higher performance renders it the first choice for small-scale, high-efficiency hydrogen production, particularly for energy and transportation fuel cells.

Additionally, as global demand for green hydrogen increases, platinum-based catalysts' scalability, stability, and existing proof of performance position them. With continuous technological innovations and the absence of substitute materials of comparable performance, platinum will continue to be in the spotlight of the hydrogen catalyst layer market.

“Asia-Pacific region is set to hold its dominant position throughout the forecast period, continuing to lead the market with strong momentum and rapid growth.”

The Asia-Pacific region is expected to remain the leading player in the hydrogen catalyst layer market due to the rapid growth in the adoption of electrolyzer technologies, favorable government policies, and expansion in hydrogen infrastructure.

Countries like China, Japan, and South Korea are heavily investing in hydrogen-based power systems and large-scale renewable energy projects, which is driving the demand for catalyst layers used in fuel cells.

China, the largest electrolyzer market in the world, is accelerating hydrogen production and the deployment of fuel cell-electric buses and trucks. Besides this, South Korea's Hydrogen Economy Roadmap and Japan's Hydrogen Society Strategy are also fueling additional market growth.

With continued technological developments and increased production capacity, the Asia-Pacific region is also expected to lead the hydrogen catalyst layer market for the foreseeable future.

Know the high-growth countries in this report. Register Here

The market is consolidated, with major players holding a significant portion of the market. Most of the major players compete in some of the governing factors, including price, product offerings, regional presence, etc. The following are the key players in the hydrogen catalyst layer market.

Here is the list of the Top Players (Based on Dominance)

Umicore

BASF SE

3M

Huntsman International LLC

Heraeus Holding

Johnson Matthey

Haldor Topsoe

Clariant

Tanaka Holdings Co., Ltd.

Nisshinbo Holdings Inc.

De Nora

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

The recent mergers & acquisitions in the market are driven by the need for advanced materials, the supply chain strengthening, and reducing production costs.

In 2024, Ecovyst Inc. (the "Company"), a leading innovative and integrated global provider of advanced materials, specialty catalysts, and services, announced an equity investment of $4.5 million in Pajarito Powder, an innovative materials science company that specializes in supports and catalysts required for electrolyzers and fuel cells.

In December 2023, Umicore started developing a new green catalyst plant. Its new greenfield plant in China is expected to become the world’s largest PEM catalyst production facility by 2030.

In 2024, scientists at Michigan State University and Princeton University created a highly stable electrocatalyst by reorganizing defective platinum diselenide (PtSe). The catalyst shows improved efficiency and lifespan, resolving cost and longevity issues in electrolyzers.

Scientists at the Daegu Gyeongbuk Institute of Science and Technology in 2024 created a catalyst made from platinum and magnesium. The new catalyst, which uses the world’s first platinum-magnesium alloy nanoparticles, is expected to be both highly efficient and durable, potentially offering significant improvements in clean energy technology.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Service portfolio, New Product Launches, etc.

COVID-19 impact and its recovery curve.

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

|

Market Study Period |

2019-2035 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2035 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

3 (Stack System Type, Base Material Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The hydrogen catalyst layer market is segmented into the following categories.

Hydrogen Catalyst Layer Market, by Stack System Type

Fuel Cell

Electrolyzer

Hydrogen Catalyst Layer Market, by Base Material Type

Platinum-based

Palladium-based

Non-Precious Metal Catalysts

Other Base Materials

Hydrogen Catalyst Layer Market, by Region

North America (Country Analysis: The USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, and Rest of Europe)

Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others)

This strategic assessment report from Stratview Research provides a comprehensive analysis that reflects today’s hydrogen catalyst layer market realities and future market possibilities for the forecast period.

The report segments and analyzes the market in the most detailed manner to provide a panoramic view of the market.

The vital data/information provided in the report can play a crucial role for market participants and investors in identifying the low-hanging fruits available in the market and formulating growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools.

More than 1,000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data.

We conducted more than 15 detailed primary interviews with market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Detailed profiling of additional market players (up to three players)

SWOT analysis of key players (up to three players)

Competitive Benchmarking

Benchmarking of key players on the following parameters: Product portfolio, geographical reach, regional presence, and strategic alliances.

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

A catalyst layer is an essential component of electrolyzer and fuel cell technologies. The layer, generally made up of well-dispersed metal catalysts (e.g., platinum, palladium, or non-precious metals) incorporated into electrodes, improves the efficiency of the reaction by supporting the water splitting in electrolyzers and electrochemical reactions in fuel cells.

The forecasted value of the hydrogen catalyst layer market is expected to be USD 9.4 billion in 2035.

The hydrogen catalyst layer market is projected to expand at a CAGR of 25.7% by 2035, fueled by advancements in material technology, the growing adoption of hydrogen-driven mobility, and environmental regulations encouraging sustainable alternatives.

The market is growing due to factors such as the rising demand for clean energy, advancements in material technology, supportive government policies, and global green hydrogen economy objectives. Furthermore, investments in renewable energy and electrolyzer-based hydrogen generation are contributing to market expansion.

Fuel cells in stack system type, Pt-based materials among base material types, and the Asia-Pacific region present significant growth opportunities during the forecast period.

The Asia-Pacific region dominates the market share, driven by the economic expansion of countries such as China, Japan, South Korea, and India, and a focus on hydrogen-based energy production and consumption.

The Asia-Pacific region is projected to experience the highest market growth, fueled by a large consumer base, government investments in sustainable energy alternatives, global carbon emission regulations, and a vast untapped market.

Umicore, BASF SE, 3M, Huntsman International LLC, Heraeus Holding, Haldor Topsoe, Johnson Matthey, Clariant, Tanaka Holdings Co., Ltd, Nisshinbo Holdings Inc., De Nora are the top players in the market.

WE ACCEPT