404

+1-313-307-4176

Fuel Cell Market Analysis | 2024-2031

Fuel Cell Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2024-2031

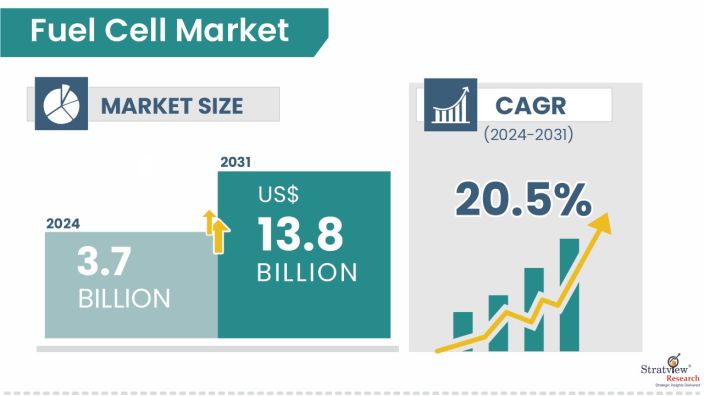

The fuel cell market size was USD 3.7 billion in 2024 and is likely to grow at a decent CAGR of 20.5% during 2024-2031 to reach USD 13.8 billion in 2031.

Want to know more about the market scope? Register Here

As industries, as well as governments, pursue cleaner, more efficient, and sustainable energy solutions worldwide, the global fuel cell market is experiencing exponential growth! Fuel cells generate electricity via an electrochemical process while offering low emissions, high efficiency, and applications in power generation, transportation, and industrial use. Due to the global push for decarbonization and renewable integration, fuel cells are expected to be essential to the hydrogen economy by providing alternatives to existing fossil-fuel-based energy systems.

The increasing technological advancements throughout hydrogen storage, distribution and production, are accelerating the adoption of fuel cells through the aforementioned end-user segments. Demonstration projects and ongoing development of infrastructure will be taking place among nations in North America, Europe, and the Asia-Pacific while developing large-scale commercialization. Private investment and increasing political support in this area are also playing a role in driving this momentum, which is creating a virtuous cycle of developing research, reducing costs, and deploying. With fuel cells progressing quickly into electric vehicles, stationary power generation, and portable devices, they will become even more central to achieving global net-zero.

The increasing emphasis on green energy transitions and decarbonization policies are key drivers for the fuel cell market. Governments around the world are adopting strict emissions norms and putting incentives in place for clean technologies that promote decarbonization, resulting in the widespread use of hydrogen-based fuel cells in transportation, energy, and industrial applications. Hydrogen production and refueling infrastructure investments are expanding as well, making the fuel cell option attractive for sustainable, large-scale energy solutions.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Cell-Type Analysis |

Proton Exchange Membrane Fuel Cells, Solid Oxide Fuel Cells, Molten Carbonate Fuel Cells, Phosphoric Acid Fuel Cells, and Other Cell Types |

Proton Exchange Membrane Fuel Cells are expected to remain dominant in the coming years. |

|

End User-Type Analysis |

Automotive & Transportation, Utilities & Power Generation, Commercial & Residential Buildings, Industrial, and Military & Defense |

The Automotive sector dominates as the largest end user of fuel cells. |

|

Application-Type Analysis |

Stationary Power Generation, Transportation, and Portable Power |

Transportation is the leading application segment throughout the forecasted period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

The Asia-Pacific is expected to maintain its reign over the forecast period. |

“Proton exchange membrane fuel cells are expected to remain dominant in the market during the forecast period.”

Proton Exchange Membrane Fuel Cells (PEMFC) are dominating the world market because of PEMFCs' efficiency, small size, and variety of applications in transportation and portable power. The major benefit of PEMFC technology is the ability to operate at relatively low temperatures, which promotes faster start-up and greater flexibility in applications for automotive and mobility. The increased focus on hydrogen-powered cars, buses, and trucks has increased investment in FDPFC, and rapid adoption by major car manufacturers has made this the most commercially mature fuel cell type.

Further, PEMFC’s commercial advantage is due to strong government incentives and R&D in decarbonising transport. Additionally, the scalability of PEMFC's technology for the stationary and small-scale applications accelerates their adoption. Although Solid Oxide Fuel Cells (SOFC) have strength in stationary power generation due to higher efficiency, fuel flexibility, and the dual benefit of lowering CO2 emissions, the PEMFC's dynamism provides a broader market reach overall. Furthermore, PEMFC's top position as the deployment fuel cell technology will be solidified as Hydrogen refueling infrastructures are developed throughout regions.

“The automotive user is expected to remain the dominant end-user of the market during the forecast period.”

The automotive industry is by far the biggest end user of fuel cells because of the increasing proliferation of hydrogen passenger and commercial vehicles. Governments are encouraging hydrogen mobility to achieve their emissions reduction target while automakers are exploring how to commercialize FCEVs at scale. It is worth noting that the automotive space enjoys a lot of policy support, subsidies, and partnerships between the fuel cell sector and vehicle manufacturers.

Utilities and commercial players are investing in fuel cell distributed power solutions, but the rate of adoption has been somewhat slower than that of all the hydrogen vehicles. Though not a large end user, the defense is also expanding into fuel cells, mainly for applications in unmanned vehicles and portable power systems. So, as it stands, the automotive industry will remain the main driver of large-scale demand for fuel cells, and hence the main end-user segment in the market.

“Transportation is expected to remain the dominant and fastest-growing application type of the market during the forecast period.”

Transportation is the largest application segment, primarily due to the rapidly growing adoption of hydrogen fuel cell vehicles (FCEVs) within commercial fleets, buses, and trucks. FCEVs offer longer driving ranges, quick refueling times, and reduced emissions compared to battery-electric vehicles while still being classified as zero-emission vehicles in heavy-duty mobility applications. All levels of government in Asia-Pacific, Europe, and North America are investing in hydrogen refueling networks to quickly commercialize hydrogen fuel cell vehicles (FCEVs) across all forms of mobility.

Stationary applications of fuel cells, such as backup power and distributed energy, are also expanding quickly, particularly in industrial and residential applications, with some success in commercial applications. However, transportation is expected to remain the largest segment for the foreseeable future as the number of hydrogen cars and buses deployed is increasing in clean mobility initiatives globally. The dominance of the transportation segment will also accelerate as automakers, such as Toyota, Hyundai, and Honda, grow their hydrogen-powered vehicle portfolios.

“Asia-Pacific is expected to remain the largest market for fuel cells during the forecast period.”

The global fuel cell market is led by the Asia-Pacific region, largely due to government policies, investment levels, and growth of hydrogen infrastructure (especially in Japan, South Korea, and China). Japan has advocated the “Hydrogen Society” concept, while South Korea and China are rapidly rolling out hydrogen buses and trucks. The region is also supported by a strong manufacturing capacity and national hydrogen roadmaps.

North America and Europe also have sizeable markets with clean energy mandates and pilot initiatives in transportation and power generation. However, the Asia-Pacific region is overwhelmingly ahead in mobility utilization, a more robust industrial ecosystem, and large infrastructure projects with government support. The conditions in the Asia-Pacific region will provide a regional hub for fuel cell innovation and commercialization.

Know the high-growth countries in this report. Register Here

The market is moderately concentrated, with over 150 players. Most of the major players compete in some of the governing factors, including price, service offerings, regional presence, etc. The following are the key players in the fuel cell market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The fuel cell market is segmented into the following categories.

By Cell Type

By End User Type

By Application Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

Fuel cell technology is an electrochemical energy conversion system that generates electricity by combining hydrogen and oxygen, producing water and heat as byproducts. Unlike combustion-based power generation, fuel cells offer high efficiency, low emissions, and scalable applications in transportation, stationary power, and portable devices.

The fuel cell market is projected to reach USD 13.8 billion by 2031, up from approximately USD 3.7 Billion in 2024, reflecting rapid adoption in transportation and clean energy sectors.

The fuel cell market is estimated to grow at a CAGR of 20.5% by 2031, driven by government decarbonization initiatives, growing demand for hydrogen mobility, and investments in hydrogen infrastructure.

Asia-Pacific holds the largest market share in the global market, led by strong government support, hydrogen infrastructure expansion, and large-scale adoption in Japan, South Korea, and China.

Ballard Power Systems, Bloom Energy, Ceres Power Holdings PLC, Doosan Fuel Cell (America), FuelCell Energy, Inc., Hydrogenics Corporation, Nedstack Fuel Cell Technology B.V., Plug Power, Inc., SFC Energy AG, and AFC Energy PLC are the leading players in the market.

WE ACCEPT