404

+1-313-307-4176

Aircraft Gearbox Market | 2025-2034

Aircraft Gearbox Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2025-2034

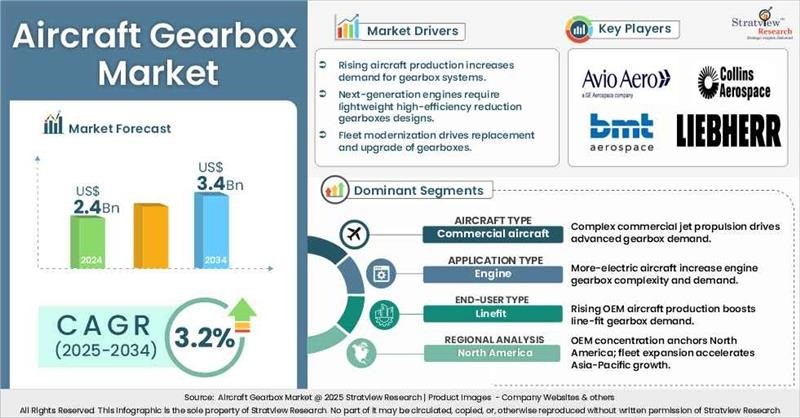

“The aircraft gearbox market size was US$2.4 billion in 2024 and is likely to grow at a decent CAGR of 3.2% in the long run to reach US$3.4 billion in 2034.”

Want to get a free sample? Register Here

Aircraft gearboxes are critical mechanical assemblies that transfer, modulate, and manage power between an aircraft engine’s main rotating shafts and the various accessories and subsystems that depend on it. These components include fuel pumps, oil pumps, hydraulic pumps, generators, starters, cooling units, and the propeller or rotor mechanisms found in turboprop and turboshaft platforms. By adjusting torque and rotational speeds, aircraft gearboxes ensure that every system mounted on the engine or airframe gets the exact mechanical input it needs for safe and efficient operation. Their design must endure extreme thermal cycles, high rotational loads, vibrations, and long hours of operation, making reliability and durability key aspects of gearbox engineering. The modern designs, spanning from accessory gearboxes (AGB), power gearbox (PGB) systems for geared turbofans, to APU gearboxes, and actuator gearboxes, showcase a trend toward greater specialization as engines evolve to feature higher bypass ratios, more-electric capabilities, and increased power density.

Market Drivers

The aircraft gearbox market is steadily growing as global manufacturing ramps up for the next generation of commercial and military platforms. With higher production rates for new turbofan families, a rising adoption of geared turbofan technology, and ongoing modernization of rotorcraft fleets, there’s a larger installed base for advanced gearbox systems. At the same time, technological advancements, such as more-electric aircraft architectures, lightweight materials, low-friction coatings, improved lubrication systems, and thermally resilient alloys, are increasing the complexity and value of gearboxes. The aftermarket is equally significant, driven by long engine life cycles, higher time-on-wing targets, and a growing demand for gearbox inspection, maintenance, and mid-life replacements. All these factors position the aircraft gearbox market for long-term growth, bolstered by rising aircraft deliveries, evolving propulsion designs, and the global expansion of fleets across commercial and military industries.

Recent Market JVs and Acquisitions:

A moderate number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Dominant and Fastest-Growing Segments |

|

Aircraft-Type Analysis |

Commercial Aircraft, Regional Aircraft, General Aviation, Military Aircraft, and Helicopter |

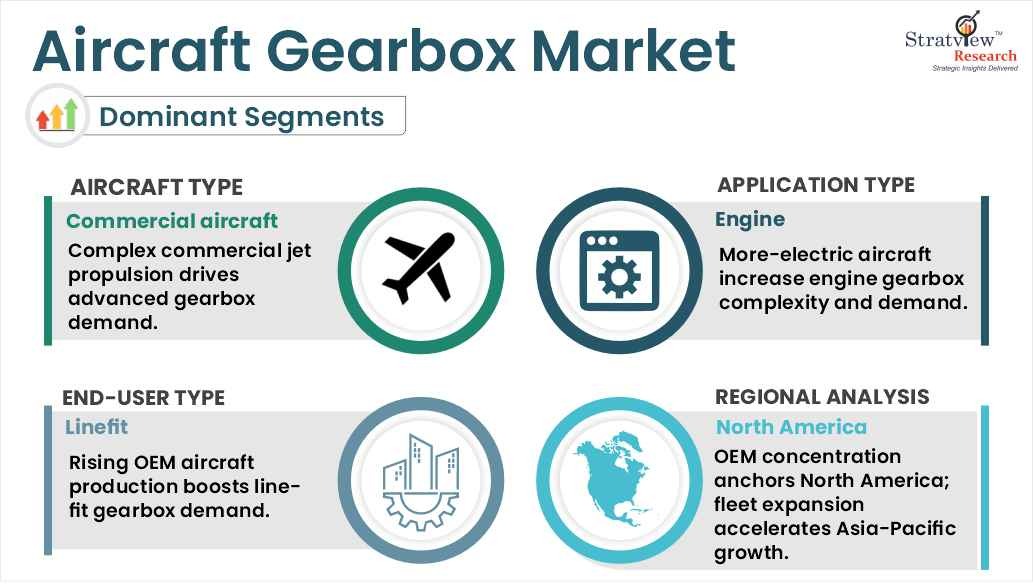

Commercial aircraft is projected to remain the dominant aircraft type throughout the forecast period. |

|

Gearbox-Type Analysis |

Accessory Gearbox, PGB, Actuator Gearbox, APU Gearbox, and Other Gearboxes |

Accessory gearboxes are anticipated to witness the fastest growth during the forecast period. |

|

Engine-Type Analysis |

Turbofan Engine, Turboprop Engine, and Other Engines |

Turbofan engines are forecasted to grow at the fastest rate among all engine types. |

|

Application-Type Analysis |

Airframe and Engine |

The engine is expected to remain the leading application of the aircraft gearbox market throughout the forecast period. |

|

End-User Type |

Linefit and Retrofit |

Line fit is projected to maintain its position as the leading end-user in the aircraft gearbox market. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is likely to retain its position as the dominant market for the aircraft gearbox throughout the forecast period. |

“Commercial aircraft is projected to remain the dominant and fastest growing aircraft type during the forecast period.”

The aircraft gearbox market is segmented by aircraft type into narrow-body aircraft, wide-body aircraft, regional aircraft, military aircraft, and general aviation.

Commercial aircraft continue to lead the global aircraft gearbox market as the dominant and fastest-growing segment. This dominance stems from the intricate and large-scale nature of their propulsion systems, which require highly specialized gearbox solutions. In contrast to regional, military, or helicopter platforms, commercial jets utilize engines that demand higher power extraction. This necessity leads to the use of multi-stage accessory gearboxes, starter-generator drives, and hydraulic or pneumatic power take-off systems.

Commercial aircraft also drives gearbox innovation, including lightweight materials, precision tooth geometries, and predictive health monitoring, which often trickles down to regional, and business jet platforms. Unlike military or helicopter gearboxes, commercial gearboxes benefit from large-scale production and fleet standardization, supporting both OEM demand and a robust aftermarket ecosystem.

Want to get a free sample? Register Here

“Accessory gearboxes are projected to remain the most widely used and the fastest-growing gearbox type throughout the forecast period.”

Based on gearbox type, the aircraft gearbox market is segmented into accessory gearbox, PGB, actuator gearbox, APU gearbox, and other gearboxes.

Accessory gearboxes are projected to remain the most widely used and fastest-growing gearbox type in the market. They play a vital role in transferring power from the engine to key systems such as fuel pumps, hydraulic actuators, electrical generators, and environmental controls, making them essential for all commercial and regional aircraft. Their growth is driven by the increasing power extraction requirements of modern turbofan and geared-turbofan engines, which require higher torque capacity, thermal durability, and a compact design. Unlike main or reduction gearboxes, accessory gearboxes need to work smoothly with various auxiliary systems, often acting as the central hub for distributing power throughout the aircraft.

This segment also benefits from the adoption of cross-platform technology, such as advancements in materials, lubrication systems, and condition-monitoring sensors for commercial jets are increasingly being used in military aircraft and rotorcraft, enhancing reliability and performance. Moreover, the move towards more electric aircraft is adding to the complexity and value of accessory gearboxes, solidifying their position in both OEM and aftermarket markets.

“Turbofan engines are expected to lead the market and are also forecast to record the fastest growth over the coming years.”

The market is segmented into the turbofan engine, turboprop engine, and other engines.

Turbofan engines are projected to dominate the aircraft gearbox market and register the fastest growth over the forecast period. Their widespread use in both commercial narrow-body and wide-body aircraft creates a strong demand for engine-mounted and accessory gearboxes, as turbofans harness power to operate high-capacity hydraulic, fuel, and electrical systems. This growth is driven by the latest high-bypass and geared-turbofan designs, which place greater torque, thermal loads, and mechanical complexity on gearboxes compared to older turbojet or turboprop engines. These increased demands call for advanced materials, precision engineering, and optimized lubrication and cooling systems, ultimately enhancing the value of each engine.

Moreover, turbofan technology is influencing adoption across various segments, like innovations in gearbox efficiency, weight reduction, and condition monitoring that were initially developed for commercial jets are now being applied to military transport, regional jets, and emerging urban air mobility platforms, boosting their market impact. The ongoing trend toward higher engine thrust-to-weight ratios and more-electric systems further solidifies turbofan gearboxes as the essential backbone of aircraft power management.

“Engines are projected to remain the leading and also the fastest-growing application throughout the forecast period.”

The market is segmented into airframe and engine.

The engine application is expected to dominate the market due to its central role in aircraft performance and reliability. Gearboxes in this application not only transfer power within the engine but also connect with various aircraft systems, such as hydraulic pumps, fuel distribution, and electrical generation. This makes engine gearboxes essential for the overall operability of aircraft, especially when compared to gearboxes used in secondary applications like landing gear or environmental control.

The growth within this segment is fueled by the increasing adoption of more-electric aircraft systems, which lead to a greater number and complexity of gearboxes linked to the engine. Additionally, engine applications significantly boost aftermarket demand, as regular maintenance, overhauls, and replacements are vital for maintaining high utilization rates in both commercial and military fleets. From a cross-segment perspective, advancements in engine gearbox reliability, monitoring systems, and material technology often benefit auxiliary gearbox applications, including helicopter, military, and regional aircraft, thereby enhancing the entire gearbox ecosystem.

“Line fit is projected to retain its leading position while also emerging as the faster-growing end-user category of the market.”

The market is segmented into linefit and retrofit.

Linefit includes gearboxes that are installed right during the aircraft assembly at OEM facilities, ensuring they integrate seamlessly and perform reliably from the very beginning of the aircraft’s operational life. The growth in this area is driven by rising production rates of commercial aircraft and the shift towards advanced engine designs and more electric systems. These innovations require gearboxes that are finely tuned for accessory drives, starter-generators, and engine-mounted systems. Unlike gearboxes installed after the fact, line-fit gearboxes are crafted for precision from the get-go and built to last, which means less maintenance and better overall performance throughout their lifecycle.

Line-fit installations also promote technology standardization across different fleets. This is a win for aftermarket service providers and makes it easier to implement retrofit or upgrade programs for regional, military, and other platforms. The linefit’s strong position is further solidified by OEMs' favoring integrated supply chains, where the early adoption of next-gen gearbox designs guarantees compatibility across various aircraft types and applications.

“North America is likely to remain the leading market for aircraft gearbox, whereas Asia-Pacific is projected to experience the fastest growth during the forecast period.”

North America remains the largest market due to its concentration of OEM and Tier-1 gearbox manufacturers, including Boeing, GE Aviation, and Pratt & Whitney. The region’s ongoing investments in engine modernization programs, particularly for narrow-body aircraft and advanced fighter jets, ensure steady demand for accessory gearboxes and drive-train components.

This region's leadership is bolstered by significant military programs, extensive commercial fleets, and ongoing engine upgrades, all of which fuel a steady demand for cutting-edge gearboxes. North American operators are also at the forefront of embracing next-generation high-bypass and geared-turbofan engines, which necessitate gearboxes that offer higher torque capacity, improved thermal management, and integrated health-monitoring systems. This positions North America not just as a high-volume market, but also as a technological benchmark for gearbox suppliers around the globe.

On the other hand, the Asia-Pacific is set to experience the highest growth. This surge is driven by the rapid expansion of commercial airline fleets, particularly with single-aisle narrow-body aircraft from major players like Airbus, Boeing, and COMAC. The region is also seeing a swift uptake of modern turbofan engines, an increase in defense procurement programs, and investments in local MRO capabilities, all of which are creating a robust demand for both OEM and aftermarket gearboxes. Moreover, Asia-Pacific is increasingly benefiting from technology transfers from North American and European OEMs, enabling local manufacturers to adopt advanced materials, high-precision gearbox designs, and predictive maintenance solutions, which in turn foster cross-segment synergies that further propel market growth.

The market is highly concentrated, with the top 5 players grabbing a huge market share. Most of the major players compete on some of the governing factors, including integration expertise with next-generation engines, proficiency in designing high-reliability gear systems, lightweighting and thermal-management innovation, durability under high rotational loads, and compliance with stringent OEM qualification cycles etc. The following are the key players in the aircraft gearbox market:

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The aircraft gearbox market is segmented into the following categories.

By Aircraft Type

By Gearbox Type

By Engine Type

By Application Type

By Application Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The aircraft gearbox market is estimated to grow at a CAGR of 3.2% by 2034, driven by rising aircraft production, delivery of fuel-efficient turbofans, and demand for lightweight, high-performance accessory drive trains and gearboxes. Advances in materials, efficiency, and stricter emission/noise regulations also support growth.

Avio Aero, BMT Aerospace, Collins Aerospace Systems, KHI, Liebherr Group, Northstar Aerospace, Safran Group, and Triumph Group Inc. are the leading players in the aircraft gearbox market.

North America is estimated to remain dominant in the aircraft gearbox market in the foreseeable future due to its strong OEM presence, engine manufacturers, and gearbox suppliers, coupled with high commercial and military aircraft production and early adoption of advanced turbofan and more-electric systems.

Asia-Pacific is estimated to remain the fastest-growing market for aircraft gearbox in the foreseeable future, mainly due to rapid fleet expansion, defense procurement, domestic aerospace programs in China, Japan, and India, and technology transfer from North America and Europe.

Engines are expected to remain the most dominant application in the market. Continuous-duty operation, high reliability, and integration with next-generation turbofans ensure strong OEM and aftermarket demand across aircraft segments.

WE ACCEPT