404

+1-313-307-4176

Automotive Simulation Market Analysis | 2025-2034

Automotive Simulation Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2025-2034

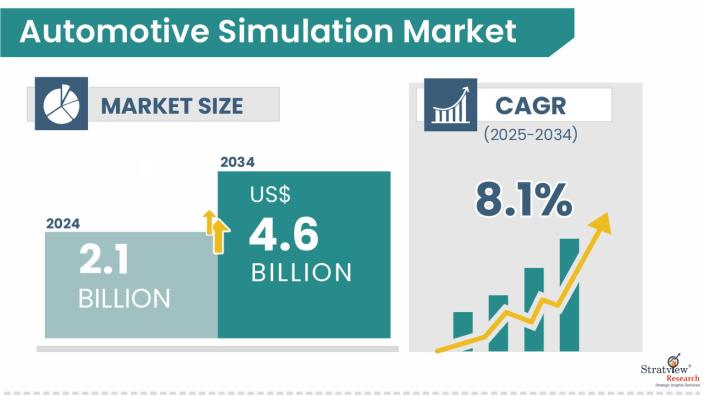

“The automotive simulation market size was USD 2.1 billion in 2024 and is likely to grow at a strong CAGR of 8.1% during 2025-2034 to reach USD 4.6 billion in 2034.”

Want to know more about the market scope? Register Here

Advanced software and technologies are used in the automobile simulation industry to produce virtual models of cars and evaluate their performance under several real-world situations. This includes simulating aspects like aerodynamics, crash safety, engine performance, and electronic systems using methods such as Computer-Aided Engineering (CAE), Finite Element Analysis (FEA), and Computational Fluid Dynamics (CFD).

As vehicles become more complex with the rise of electric, autonomous, and connected technologies, simulation helps manufacturers design and test vehicles more efficiently, reducing the need for costly physical prototypes. It supports faster product development, improved safety, and regulatory compliance.

Increasing need for creativity, cost cutting, and regulatory criteria in the automobile industry drives the market. It enables companies to virtually explore multiple design options, optimize performance, and identify potential issues early in the development process, making simulation an essential part of modern vehicle engineering.

Recent trends in joint ventures and acquisitions within the automotive simulation market reflect a strategic shift toward collaborative innovation and technological integration. Leading companies are forming alliances to co-develop advanced simulation platforms, particularly focusing on software-defined vehicles (SDVs) and autonomous driving technologies. These partnerships aim to leverage combined expertise to accelerate development cycles, enhance system interoperability, and reduce costs. Additionally, there is a notable increase in acquisitions targeting specialized simulation firms, enabling larger entities to expand their capabilities in areas such as AI-driven modelling, digital twins, and cloud-based simulation services. This consolidation trend is driven by the need to offer comprehensive, end-to-end solutions that address the growing complexity of modern vehicle systems. Overall, the market is experiencing a dynamic evolution, characterized by strategic collaborations and acquisitions that are reshaping the landscape of automotive simulation.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Deployment-Type Analysis |

On-premises and Cloud |

On-premises is expected to continue its dominance during the forecast period due to the high security, control, and customization offerings. |

|

Application-Type Analysis |

Drive Systems, Mechanical Components, and Fluid Power |

Fluid Power is anticipated to exhibit the highest growth rate throughout the forecast period, driven by the rising complexity of hydraulic systems in modern vehicles. |

|

End-User Type Analysis |

OEM and Suppliers |

OEM is expected to dominate the market during the forecast period due to heavy investments in simulation technologies. |

|

Component-Type Analysis |

Software and Services |

Services are anticipated to exhibit the highest CAGR throughout the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

Asia-Pacific is expected to dominate as well as experience the highest growth rate throughout the forecast period. |

“The on-premises category is expected to continue to dominate the market during the forecast period.”

Based on the deployment, the market is segmented into on-premises and cloud. The on-premises segment is expected to continue to dominate the market in terms of revenue, largely due to the high security, control, and customization it offers, which are critical for large automotive manufacturers managing complex simulations in-house. Meanwhile, the cloud-based segment is expected to register the highest CAGR during the forecast period. This growth is driven by the increasing adoption of cloud computing, remote collaboration needs, and the rise of startups and smaller firms that prefer cost-effective, scalable solutions.

“The fluid power application is anticipated to exhibit the highest growth rate throughout the forecast period.”

Based on the application, the market is segmented into drive systems, mechanical components, and fluid power. Among these, the drive systems category is expected to remain dominant due to the increasing demand for rapid prototyping in vehicle development, allowing manufacturers to analyse and refine new product behaviours efficiently before transitioning to mass production. Whereas the fluid power segment is expected to experience the highest growth rate during the forecast period, driven by the rising complexity of hydraulic systems in modern vehicles, including applications in braking, steering, and suspension systems.

“The OEM (Original Equipment Manufacturer) segment is expected to dominate throughout the forecast period.”

Based on the end-user type, the market is segmented into OEM and suppliers. The OEM (Original Equipment Manufacturer) segment is expected to dominate the market in terms of market share during the forecast period. OEMs heavily invest in simulation technologies to accelerate vehicle development, reduce prototype costs, and meet strict regulatory and safety standards. On the other hand, the supplier segment is expected to experience the highest CAGR throughout the forecast period. This is driven by the increasing role of Tier-1 and Tier-2 suppliers in developing and integrating advanced vehicle components, such as sensors, ADAS systems, and electric drivetrains, which require rigorous simulation and validation before integration into OEM platforms.

“The software is expected to dominate during the forecast period.”

Based on the component, the market is segmented into software and services. The software segment is expected to dominate the market in terms of market share throughout the forecast period, primarily due to the increasing adoption of simulation software for designing, testing, and validating various automotive components virtually, which helps in reducing development time and cost. The services segment, on the other hand, is expected to experience the highest CAGR during the forecast period. This growth is driven by the rising demand for consulting, integration, support, and maintenance services as OEMs and suppliers increasingly rely on simulation experts to customize and optimize their simulation workflows.

“The Asia-Pacific region is expected to both dominate and grow at the highest CAGR in the market during the forecast period.”

Asia-Pacific is expected to dominate the automotive simulation market in terms of market size as well as experience the highest growth rate throughout the forecast period. This growth is driven by factors such as the rapid expansion of the automotive industry, increasing investments in electric and autonomous vehicle development, and the presence of major automotive manufacturers in countries like China, Japan, and South Korea.

Know the high-growth countries in this report. Register Here

The market consists of a considerable number of players, featuring several key players renowned for their expertise and contributions. The following are the key players in the automotive simulation market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The automotive simulation market is segmented into the following categories.

By Deployment Type

By Application Type

By End-User Type

By Component Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

Automotive simulation is the process of using computer-based models and software tools to virtually replicate and analyze the behavior, performance, and interactions of a vehicle or its components under various real-world conditions. It involves simulating physical phenomena such as aerodynamics, crash impacts, thermal dynamics, powertrain performance, vehicle dynamics, and electronic system behavior. These simulations help engineers and manufacturers design, test, and optimize vehicles without the need for physical prototypes, thereby saving time, reducing costs, and improving safety and efficiency.

The forecasted value for the market is USD 4.6 billion in 2034.

The market is estimated to grow at a CAGR of 8.1% by 2034.

Asia-Pacific currently holds the largest market share and is expected to continue its dominance.

ANSYS Inc., Siemens Digital Industries Software, Dassault Systèmes, Altair Engineering Inc., MSC Software, ESI Group, and Autodesk Inc.

WE ACCEPT