404

+1-313-307-4176

Bifacial Solar Panels Market Report

Bifacial Solar Panels Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2024-2031

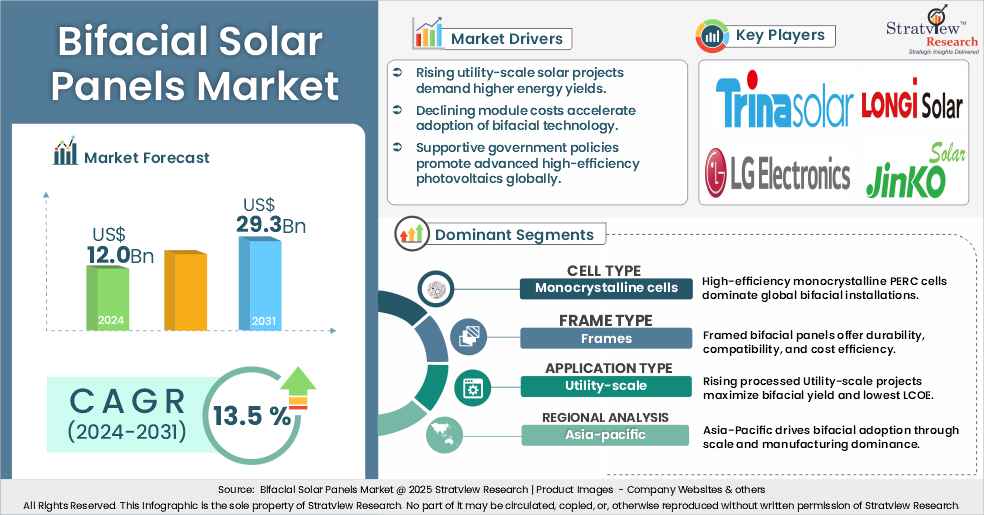

“The bifacial solar panels market size was US$12.0 billion in 2024 and is likely to grow at a decent CAGR of 13.5 % in the long run to reach US$29.3 billion in 2031.”

Want to get a free sample? Register Here

Introduction

The bifacial solar panel market is developing quite rapidly in the worldwide renewable energy market because these panels can generate electricity from both their front and rear sides. Bifacial modules can generate 10-30% more energy than a standard monofacial panel by capturing reflected sunlight off various locations, such as the ground or rooftops. The difference in energy yield (additional energy yield) dramatically enhances the economics of a project (notably utility-scale solar farms), particularly in high albedo settings (white, or highly reflective surfaces). Solar developers are more focused than ever on maximizing output per square meter, and bifacial panels are part of the strategy.

Recent advancements in cell technologies, namely PERC, TOPCon, and HJT, have also coincided with the increased utilization of bifacial modules, in addition to the supportive policy environment and declining costs. Installations in 2020 and 2021 were led by China, the U.S., India, and some countries in the Middle East that have aggressive renewable energy targets and the availability of large areas of land. Additionally, the pairing of bifacial panels with single-axis trackers is resulting in a significant increase in output gain, especially in sunny desert-like areas. Therefore, bifacial technology is appearing to be the next step in terms of solar PV.

Market Driver:

The increasing demand for high-efficiency and low-cost renewable energy systems supporting the global goal of carbon neutrality remains a key opportunity for the bifacial solar panel market. Bifacial modules support higher energy yield without an increase in installation costs, providing a very competitive advantage in regions achieving grid parity. This is particularly relevant for utility-scale developers who are focused on maximizing return on investment (ROI) and maintaining long-term system performance.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Cell-Type Analysis |

Monocrystalline, Polycrystalline, Passivated Emitter Rear Cell, and Heterojunction Technology |

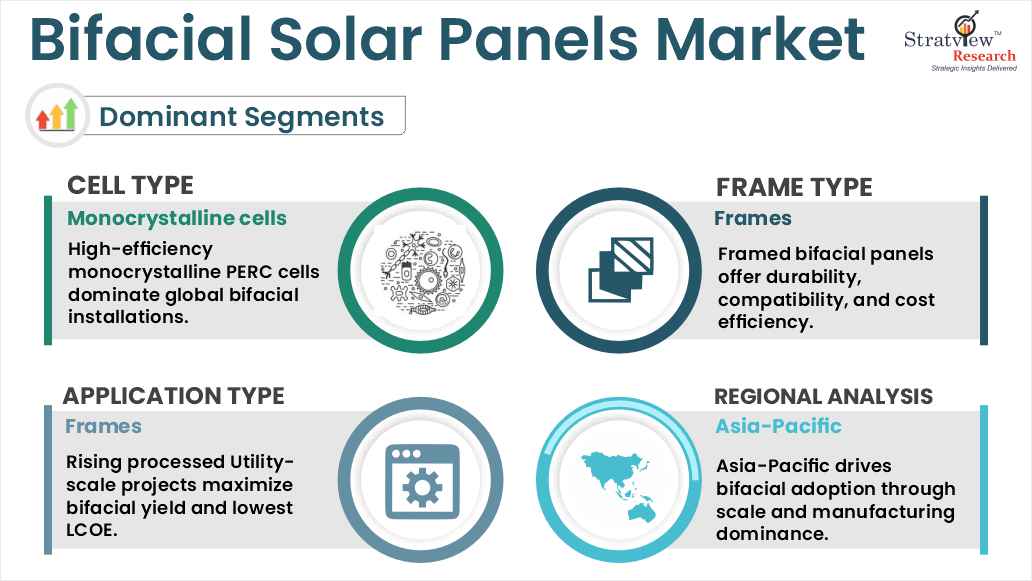

Monocrystalline cells are expected to remain dominant in the coming years. |

|

Frame-Type Analysis |

Framed and Frameless |

Frames are anticipated to hold the largest share of the market in the upcoming years. |

|

Application-Type Analysis |

Utility-scale, Commercial & Industrial, and Residential |

Utility-scale applications are expected to be the dominant type in the market in the forecasted period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

The Asia-Pacific is expected to maintain its reign over the forecast period. |

By Cell Type

“Monocrystalline cells are expected to remain dominant in the market during the forecast period.”

Monocrystalline bifacial panels, particularly those utilizing PERC (Passivated Emitter Rear Contact) technology, lead the market in terms of efficiency, longevity, and reduced production costs. PERC cells are more effective than polycrystalline under conditions of low light and high ambient temperature—important characteristics and considerations for large utility-style applications across various climates.

While there has been much development of alternatives from TOPCon and HJT structures, monocrystalline PERC is still the mass-market option, supported by larger manufacturing facilities with brownfield sites, lower capex with less sophisticated equipment, and greater experience in development and deployment. They are more bifacial than typical polycrystalline, making them the standard for new installations around the world, particularly in the Asia-Pacific region, as well as the U.S.

By Frame Type

“Framed type is expected to be the dominant in the market during the forecast period.”

Due to their structural support, ease of handling, and installation costs, framed bifacial panels lead the way. They are much more compatible with the existing mounting/racking systems, needing any custom BOS (Balance of System) components.

There are advantages to frameless panels in aesthetics and lighter weight, but they are mostly used for niche architectural projects or BIPV (Building Integrated PV), whereas framed panels are ruggedized and designed for large-scale, high-load situations such as deserts or snowy environments. The applicability of framed panels to the mass market is the reason they are the preferred product for solar farm developers.

By Application Type

“Utility scale is expected to be the dominant and fastest-growing application of the market during the forecast period.”

Utility-scale projects are clearly the most common use for bifacial solar panels, as these projects allow for the most energy yield and the lowest levelized cost of electricity (LCOE). Utility sites have a larger area to work with and reflective surfaces that approximately double the amount of backside irradiance than rooftops, which would make it much easier to optimize bifacial gain.

In addition, utility developers are combining bifacial with single-axis trackers, resulting in maximizing backside access to the sun. We are seeing better long-term performance as a result of these two components working together, which further drives investments. Lastly, as significant investments are being made by governments and large corporations into grid-scale renewables, utility-scale is still going to be the most profitable and most scalable application for bifacial systems.

Want to get more details about the segmentations? Register Here

Regional Analysis

“The Asia-Pacific is expected to remain the largest market for Bifacial Solar Panels during the forecast period.”

Asia-Pacific leads the bifacial solar panel market due to fierce renewable targets, cost-competitive manufacturing, and large deployment in both China and India. The bifacial solar panel market is skewed by China and provides a large market share based on local incentives, sites with high albedo from the sun in the northwest, and large players like Trina and LONGi.

While China is the largest investor in bifacial solar technology, the entire Asia-Pacific region has ample domestic supply chains and a financing environment that facilitates and accelerates the adoption of this technology. Factors in the region related to climate, increasing energy demand, and solar investment pipelines are also ideal for scaling the technology of bifacial solar. The Asia-Pacific region is still the primary driver of growth, both on the production and installation side.

The market is moderately concentrated, with over 100 players. Most of the major players compete in some of the governing factors, including price, service offerings, regional presence, etc. The following are the key players in the Bifacial Solar Panels market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

The global Bifacial Solar Panels market is segmented into the following categories.

Bifacial Solar Panels Market, by Cell Type

Bifacial Solar Panels Market by Frame Type

Bifacial Solar Panels Market by Application Type

Bifacial Solar Panels Market by Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

Bifacial solar panels are photovoltaic modules that can capture sunlight from both the front and rear sides, increasing total energy generation. The rear side absorbs reflected sunlight (albedo) from the ground or surrounding surfaces, leading to 10–30% more energy output compared to traditional monofacial panels. They are commonly made with glass-glass or glass-transparent backsheet designs and are especially effective when mounted on reflective surfaces.

The global bifacial solar panel market is projected to reach approximately US$29.32 billion by 2031, growing from US$12.08 billion in 2024.

The Bifacial Solar Panels market is estimated to grow at a CAGR of 13.5% by 2031, driven by increased demand for high-efficiency PV systems, technological advancements like TOPCon and HJT, and supportive government renewable energy policies.

High-growth segments include monocrystalline (PERC) cell types, utility-scale applications, and Asia-Pacific deployments, where high albedo conditions and large solar investments accelerate adoption.

Asia-Pacific holds the largest share of the bifacial solar panel market, led by massive installations and production capabilities in countries like China, India, and Japan.

Trina Solar, LONGi Solar, JinkoSolar, LG Electronics, Panasonic, Canadian Solar, Yingli Green Energy, SolarWorld, MegaCell, and Lumos Solar are the leading players in the Bifacial Solar Panels market.

WE ACCEPT