404

+1-313-307-4176

Robotic Warfare Market Report

Robotic Warfare Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2025-2032.

Want to get a free sample? Register Here

Have a look at the sales opportunities presented by the robotic warfare market in terms of growth and market forecast.

|

Robotic Warfare Market Data & Statistics |

|

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

|

Annual Market Size in 2023 |

USD 30.19 billion |

- |

|

|

Annual Market Size in 2024 |

USD 32 billion |

YoY Growth in 2024: 6% |

|

|

Annual Market Size in 2025 |

USD 33.97 billion |

YoY Growth in 2025: 6.15% |

|

|

Annual Market Size in 2032 |

USD 50.91 billion |

CAGR 2025-2032: 5.95% |

|

|

Cumulative Sales Opportunity during 2025-2032 |

USD 336.15 billion |

- |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 25 billion + |

> 80% |

|

|

Top 10 Company’s Market Share in 2024 |

USD 16 billion to USD 22 billion |

50% - 70% |

|

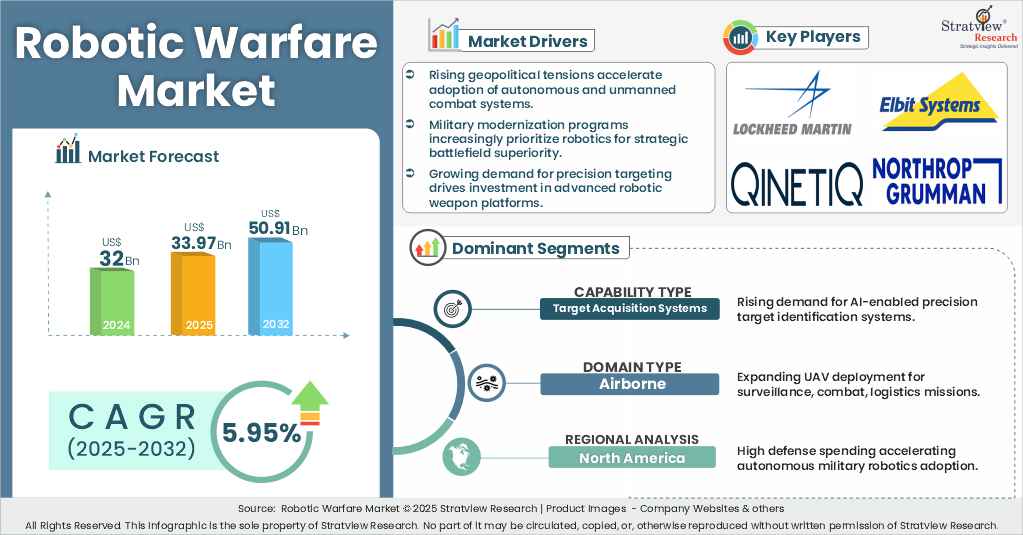

What is robotic warfare?

Robotic warfare refers to the use of autonomous and semi-autonomous robotic systems in military operations. These systems include unmanned aerial vehicles (UAVs), ground robots (UGVs), marine drones, weaponized turrets, and exoskeletons designed to enhance combat capabilities, reduce human risk, and improve mission efficiency. Robotic warfare technologies are widely used in intelligence, surveillance, and reconnaissance (ISR), combat operations, logistics and support, and search and rescue missions across land, air, and naval domains.

Increasing Development and Deployment of AI-Driven Robotic Systems

High Development Costs, Integration Complexities

Increasing Adoption of Autonomous Training and Simulation

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Application Analysis |

Intelligence, Surveillance, & Reconnaissance (ISR), Logistics & Support, Search & Rescue, Tracking & Targeting, Combat & Operations, Training & Simulation |

ISR segment is expected to grow at the highest CAGR during the forecast period.

|

|

Capability Analysis |

Unmanned Platforms & Systems, Exoskeleton & Wearables, Target Acquisition Systems, Turret & Weapon System |

Target Acquisition Systems segment is expected to grow at a faster pace during the forecast period.

|

|

Domain Analysis |

Land, Marine, Airborn |

Airborne segment holds the largest market revenue and is anticipated to grow at the highest CAGR during the forecast period. |

|

Mode of Operation Analysis |

Autonomous, Semi-Autonomous |

Semi-Autonomous segment is projected to grow at the highest CAGR during the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America holds the largest share of the robotic warfare market. |

“Target Acquisition Systems segment is expected to grow at a faster pace during the forecast period.”

“Airborne segment holds the largest market revenue and is anticipated to grow at the highest CAGR during the forecast period.”

Want to get more details about the segmentations? Register Here

“North America holds the largest share of the robotic warfare market.”

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the robotic warfare market -

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

|

Market Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

5 (Application Type, Capability Type, Domain Type, Mode of Operation Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

This report studies the market, covering a period of 15 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The robotic warfare market is segmented into the following categories.

Global Robotic Warfare Market, by Application Type

Global Robotic Warfare Market, by Capability Type

Global Robotic Warfare Market, by Domain Type

Global Robotic Warfare Market, by Mode of Operation Type

Robotic Warfare Market, by Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The global robotic warfare market refers to the industry centered around the development, deployment, and integration of robotic systems in military and defense operations. These systems include unmanned ground vehicles (UGVs), unmanned aerial vehicles (UAVs), autonomous naval drones, combat robots, AI-driven target acquisition systems, and robotic exoskeletons.

The forecasted value for the market is US$50.91 billion in 2032.

The robotic warfare market size was USD 32 billion in 2024 and is expected to grow from USD 33.97 billion in 2025 to USD 50.91 billion in 2032, witnessing an impressive market growth (CAGR) of 5.95% during the forecast period (2025-2032).

The key drivers of the global robotic warfare market are the increasing development and deployment of AI-driven robotic systems, increasing adoption of autonomous training and simulation.

The top players in the global robotic warfare market include Elbit Systems Ltd., Lockheed Martin Corporation, Northrop Grumman Corporation, Rheinmetall AG, QinetiQ, etc.

North America holds the largest share of the robotic warfare market.

WE ACCEPT