404

+1-313-307-4176

Aircraft Fuel Valves Market Report

Aircraft Fuel Valves Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2024-2034

Aircraft Fuel Valves Market is segmented by Aircraft Type (Commercial Aircraft, General Aviation, Regional Aircraft, Military Aircraft, Helicopter and Unmanned Air Vehicle), by Valve Type (Hand Operated Valves, Manually Operated Gate Valves, Motor Operated Valves, Solenoid Operated Valves, and Other Valves), by Material Type (Stainless Steel, Titanium, Aluminium, and Composites), by End-User Type (OEM and Aftermarket), and by Region (North America [The USA, Canada, and Mexico], Europe [Germany, France, The UK, Russia, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], and Rest of the World [Brazil, Saudi Arabia, and Others]).

“The aircraft fuel valves market was valued at US$ 99.1 million in 2024 and is likely to grow at a decent CAGR of 4.0% in the long run to reach US$ 155.6 million in 2034.”

Want to know more about the market scope? Register Here

Aircraft fuel valves are critical components used to regulate and control the flow of fuel within an aircraft’s fuel system, ensuring safe and efficient engine operation. These valves play a vital role in isolating fuel tanks, managing fuel supply to the engine, and supporting emergency shut-off functions. As aircraft fuel systems become more complex with advancements in engine technologies and fuel efficiency standards, the demand for precise and reliable fuel valve systems has grown substantially. Fuel valves are exclusively used in the engine application segment and are engineered to withstand extreme pressure, vibration, and temperature conditions, making material selection and design paramount in their development.

The aircraft fuel valves market is poised for significant growth, driven by the continuous rise in global air traffic, expansion of commercial and regional aircraft fleets, and increasing military aircraft modernization programs. Additionally, the growing focus on fuel system efficiency and engine safety has compelled OEMs and system integrators to invest in advanced, lightweight, and corrosion-resistant fuel valve technologies.

In summary, the aircraft fuel valves market is evolving in tandem with advancements in propulsion systems and aircraft design, as manufacturers aim to enhance fuel delivery precision, reduce system weight, and comply with stringent safety regulations. With the increasing emphasis on operational reliability and lifecycle cost-effectiveness, the market is expected to witness steady innovation and growth in the coming years.

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Aircraft-Type Analysis |

Commercial Aircraft, General Aviation, Regional Aircraft, Military Aircraft, Helicopter, and Unmanned Air Vehicle |

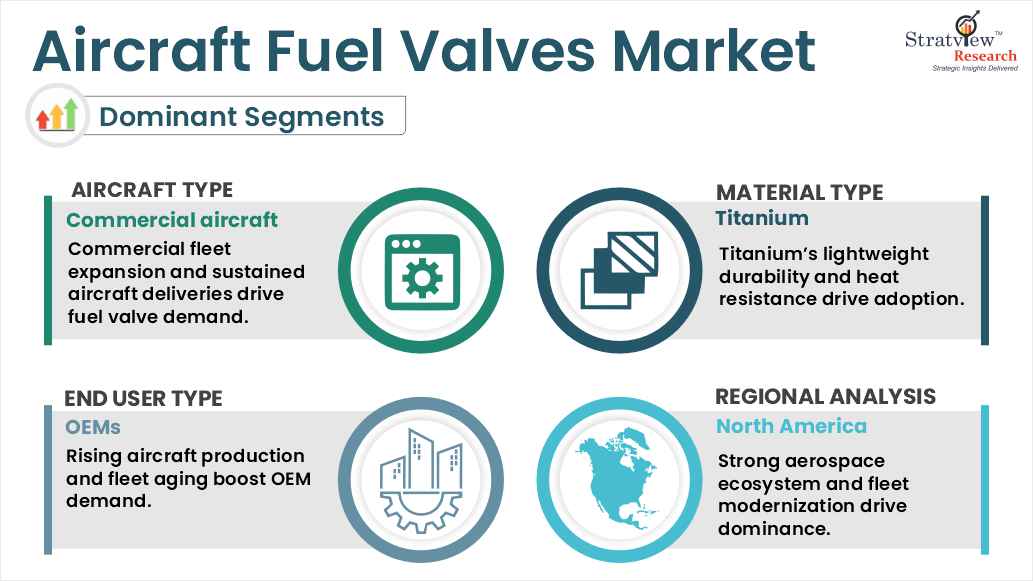

Commercial aircraft are expected to hold the major share of the market and are also likely to be the fastest-growing segment during the forecast period. |

|

Valves-Type Analysis |

Hand Operated Valves, Manually Operated Gate Valves, Motor Operated Valves, Solenoid Operated Valves, and Other Valves |

Solenoid-operated valves are anticipated to be the dominant valve type in the market during the forecast period. |

|

Material-Type Analysis |

Stainless Steel, Titanium, Aluminium, and Composites |

Titanium is anticipated to account for the largest market share, while composites are expected to be the fastest-growing material type during the forecast period. |

|

End-User-Type Analysis |

OEM and Aftermarket |

OEMs are expected to drive most of the demand, while the aftermarket segment is likely to experience the fastest growth in the coming years. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to maintain its reign over the forecast period, whereas Asia-Pacific is likely to grow at the fastest rate. |

“Commercial aircraft are anticipated to be the biggest demand generator of the aircraft fuel valves market during the forecast period.”

The aircraft fuel valves market is categorized by aircraft type into commercial aircraft, general aviation, regional aircraft, military aircraft, helicopters, and unmanned aerial vehicles (UAVs).

The commercial aircraft segment is expected to remain the primary demand driver for the aircraft fuel valves market over the forecast period. This dominance stems from the consistent growth in global air passenger traffic and the robust pipeline of new aircraft deliveries planned by major commercial airlines worldwide. According to the latest market outlooks from Boeing and Airbus, over 42,000 new commercial aircraft are projected to be delivered over the next two decades. These large-scale production targets reflect a confident industry outlook centered around fleet expansion, aircraft replacement, and increasing connectivity across emerging and developed regions.

As the number of commercial aircraft in operation continues to rise, so does the demand for efficient and reliable fuel system components, especially fuel valves, which are critical to engine performance, fuel flow management, and safety compliance. Commercial aircraft typically operate on long-haul and high-frequency routes, requiring fuel systems that are both robust and precise. Aircraft fuel valves used in these platforms must meet stringent performance standards and undergo rigorous quality control to ensure reliable operation under extreme flight conditions.

Furthermore, the extensive backlogs recorded by major OEMs, nearly 14,849 aircraft as of early 2025, indicate a sustained production pace that directly feeds into the demand for OEM-supplied fuel valve systems. At the same time, the growing size and aging of the global commercial fleet create a parallel opportunity in the aftermarket segment, where fuel valves must be routinely inspected, replaced, or upgraded to maintain operational safety and efficiency. These factors collectively position the commercial aircraft segment as the largest and most influential contributor to the growth of the aircraft fuel valves market.

“Solenoid-operated valves are likely to hold the major share in the aircraft fuel valves market during the forecast period.”

Based on valves type, the aircraft fuel valves market is segmented as hand-operated valves, manually operated gate valves, motor-operated valves, solenoid-operated valves, and other valves.

Solenoid-operated valves are projected to dominate the aircraft fuel valves market due to their rapid response and precise control, which are essential in critical engine fuel applications. These valves can actuate in milliseconds, allowing for near-instantaneous fuel flow adjustments essential during engine start, shutdown, and emergency fuel isolation. Their electrical actuation provides consistent on/off control, meeting stringent safety and performance requirements in aircraft fuel systems.

Furthermore, solenoid valves offer high reliability with low maintenance requirements. With fewer mechanical parts, they experience less wear and tear, thereby reducing the frequency of inspections and replacements. Constructed from durable materials such as stainless steel, these valves perform reliably under extreme temperature and vibration conditions commonly encountered in flight.

Finally, solenoids are energy-efficient and automation-ready, consuming power only during state transitions and remaining passive while holding position. This efficiency aligns well with modern aircraft systems' demand for low-power components. Moreover, electrical actuation simplifies system integration, enabling seamless collective control via onboard automation systems like FADEC (Full Authority Digital Engine Control).

“Titanium is likely to be the dominant material type, whereas composites will emerge as the fastest-growing material type in the market during the forecast period.”

By material type, the aircraft fuel valves market is segmented into stainless steel, titanium, aluminium, and composites.

Titanium stands out as the dominant material for aircraft fuel valves during the forecast period, owing to its exceptional strength-to-weight ratio, corrosion resistance, and high-temperature performance. In aerospace applications, these properties allow titanium valves to be both lightweight and capable of withstanding the extreme conditions of engine environments, such as high pressure and heat, attributes that aluminum and stainless steel cannot match. While titanium is more expensive and requires specialized manufacturing, ongoing advancements in alloy development and additive manufacturing are improving its cost-efficiency and availability. Consequently, titanium remains the preferred choice for high-performance fuel valves critical to commercial, military, and advanced aircraft fleets.

Composites, on the other hand, are emerging as the fastest-growing material segment in the aircraft fuel valves market. Carbon-fiber reinforced composites offer an unrivaled combination of ultra-low weight, high fatigue strength, and excellent corrosion resistance, making them highly appealing for weight-sensitive aerospace components. While traditionally confined to airframes and structural parts, more sophisticated composites are now being adapted for complex, small-scale functional components, such as brackets, fasteners, and potentially valve bodies, supported by continuous innovations in manufacturing that enhance affordability and scalability.

Want to get more details about the segmentations? Click Here

“OEMs are projected to be the dominant end-user, whereas the aftermarket segment is poised for faster growth in the market throughout the forecast period.”

The aircraft fuel valves market is segmented by end user into OEM and aftermarket. The OEMs (Original Equipment Manufacturers) are expected to remain the dominant end-users in the aircraft fuel valves market throughout the forecast period. This dominance is primarily driven by the continuous production of new aircraft. As airlines expand fleets and upgrade to newer models, OEMs supply integrated fuel valve systems directly during aircraft manufacturing. Major OEMs, including Boeing and Airbus, forecast a multi-decade delivery pipeline of tens of thousands of new aircraft, underpinning demand for first-fit components like fuel valves. Moreover, OEMs retain control over product design, quality standards, and certification, giving them a clear advantage in the supply chain.

In contrast, the aftermarket segment is set to experience the fastest growth over the forecast horizon. This surge is powered by the rapidly expanding global aircraft fleet and the aging of existing aircraft, which fuels the demand for replacement, maintenance, repair, and overhaul (MRO) services. Maintenance cycles and valve replacement intervals, known to be relatively frequent, also support aftermarket demand. OEMs themselves are increasingly participating in MRO services, while independent shops offer cost-competitive alternatives. As airlines prioritize reducing downtime and maintenance costs, aftermarket suppliers that can provide certified, lightweight, and high-performance fuel valves are gaining market share.

“North America is expected to retain its dominant position throughout the forecast period, while Asia-Pacific is projected to grow at the fastest rate.”

North America is poised to hold the major share of the aircraft fuel valves market, due to its well-established aerospace ecosystem. With major aircraft manufacturers and system integrators like Boeing, Collins Aerospace, Honeywell, and Parker Hannifin rooted in the USA and Canada, a robust foundation supports continuous R&D, production, and modernization of fuel systems. The region’s strong commercial and defense aviation industries further drive demand, not only for new aircraft but also for retrofitting and upgrading existing fleets with innovative fuel valve technologies like SAF-compatible and digital-control valves.

Moreover, North America’s advanced regulatory frameworks and commitment to sustainable aviation systems promote early adoption of cutting-edge materials and valve designs. Substantial investments in modernizing aging fleets and developing next-gen engines reinforce the demand for high-performance fuel valves, solidifying North America’s leadership in market share and technological innovation for the duration of the forecast period.

Meanwhile, the Asia–Pacific is on track to experience the fastest growth in the aircraft fuel valves market. This surge is fueled by explosive growth in air travel, propelled by rising middle-class incomes, tourism, and rapid urbanization in countries like China, India, Japan, Australia, and Southeast Asian nations. China, India, and Southeast Asia are not only expanding airline fleets but also investing heavily in airport infrastructure, which supports both OEM deliveries and fuel system demands.

The market is consolidated, dominated by a few large multinational OEM-tier suppliers. The following are the key players in the aircraft fuel valves market.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aircraft fuel valves market is segmented into the following categories.

By Aircraft Type

By Valve Type

By Material Type

By End-User Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Aircraft fuel valves are precision-engineered components within an aircraft’s fuel system that control the flow, direction, and isolation of fuel between tanks and engines. They perform critical functions like fuel shut-off during emergencies, selecting specific tanks for engine supply, enabling cross-feed between multiple tanks, and managing refueling or defueling operations. Common types include shut-off valves, selector valves, cross-feed valves, and dump/refuel valves, each designed to meet high standards for safety, reliability, and performance. These valves ensure engines receive a steady, contamination-free fuel flow at precise pressure and volume, even under extreme flight conditions such as varying altitudes, temperatures, and vibrations.

The aircraft fuel valves market is projected to grow at a CAGR of 4.0% over the coming years, reaching a value of US$ 155.6 million by 2034.

The aircraft fuel valves market is primarily driven by rapid growth in global air traffic and aircraft deliveries, as rising passenger and cargo demand propels airlines to expand and modernize their fleets. A strong emphasis on fuel efficiency and environmental sustainability further fuels demand, and aircraft operators seek lightweight, high-performance valve systems compatible with sustainable aviation fuels (SAF) and hybrid-electric propulsion technologies. Additionally, technological advancements in materials, design, and smart valve technologies, such as IoT-enabled and predictive-maintenance systems, are enabling more reliable, compact, and efficient valves. The market is also supported by increased defense spending, which expands demand for military aircraft fuel systems and UAVs. Finally, stringent regulatory standards and safety requirements from agencies like the FAA and EASA ensure ongoing upgrades and replacements, maintaining demand for certified, high-precision fuel valves.

North America holds the largest share in the global aircraft fuel valves market, driven primarily by the presence of major aircraft OEMs such as Boeing, Lockheed Martin, and Raytheon Technologies, along with a well-established aerospace supply chain. The region benefits from strong government and defence spending, continuous investments in aerospace innovation, and a high rate of aircraft production and maintenance activities. Additionally, the large commercial aircraft fleet and the rising demand for technologically advanced fuel systems further contribute to the region’s market dominance. The presence of key valve manufacturers and a strong focus on performance, safety, and regulatory compliance continues to reinforce North America’s leadership position in this segment.

Asia-Pacific is emerging as the fastest-growing market for aircraft fuel valves, fuelled by rapid growth in commercial aviation, rising defence budgets, and expanding aircraft fleets across countries such as China, India, and Japan. The region is witnessing significant investments in new aircraft manufacturing and maintenance infrastructure, along with an increasing number of low-cost carriers and air travel demand from a growing middle-class population. Government initiatives to boost domestic aerospace capabilities and joint ventures with global OEMs are further accelerating market growth. As aerospace & defence industries modernize their fleets, the need for efficient and high-performance fuel systems, including valves, continues to surge.

Parker Hannifin Corporation, Safran S.A., Woodward, Inc., and Transdigm Group Inc. are the leading players in the aircraft fuel valves market.

WE ACCEPT