404

+1-313-307-4176

Hyperscale Data Center Market | 2025-2032

Hyperscale Data Center Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2025-2032

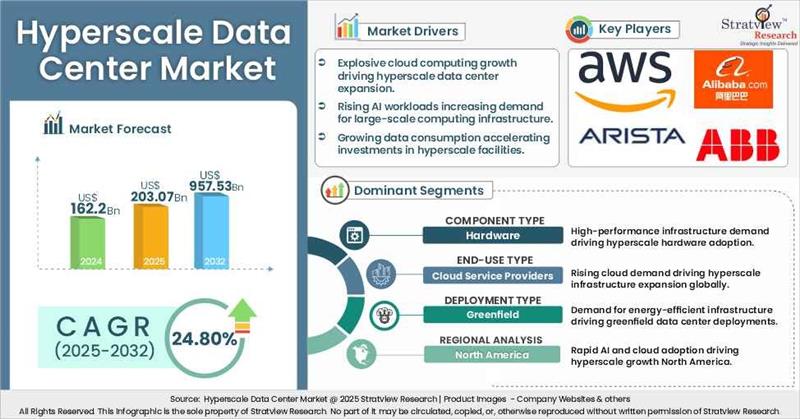

"hyperscale data center market size was USD 162.2 billion in 2024.”

Want to get a free sample? Register Here

Have a look at the sales opportunities presented by the hyperscale data center market in terms of growth and market forecast.

Hyperscale Data Center Market Data & Statistics

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

Annual Market Size in 2023 |

USD 133.17 billion |

|

|

Annual Market Size in 2024 |

USD 162.2 billion |

YoY Growth in 2024: 21.80% |

|

Annual Market Size in 2025 |

USD 203.7 billion |

YoY Growth in 2025: 25.20% |

|

Annual Market Size in 2032 |

USD 957.13 billion |

CAGR 2025-2032: 24.80% |

|

Cumulative Sales Opportunity during 2025-2032 |

USD 4010.19 billion |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 129.76 billion + |

> 80% |

|

Top 10 Company’s Market Share in 2024 |

USD 81.10 billion to USD 113.54 billion |

50% - 70% |

What is hyperscale data center?

Hyperscale data centers are powerhouses for the modern internet, enabling the massive computational power required for cloud computing, artificial intelligence, streaming services, and global digital infrastructure. Unlike traditional data centers, these mega-scale facilities are designed for extreme scalability, energy efficiency, and high-speed connectivity, supporting the exponential growth of data consumption worldwide. The hyperscale data center market is undergoing exceptional growth, powered by the demand for AI, cloud computing, and 5G-driven edge applications. Hyperscalers like AWS, Google Cloud, Microsoft Azure, and Meta are leading the expansion and deployment of energy-efficient facilities to support next-gen workloads.

Exponential Growth in Cloud Computing & AI Workloads:

High Energy consumption and Capacity Challenges:

Expansion of 5G Infrastructure:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Component Type Analysis |

Hardware, Software, and Services |

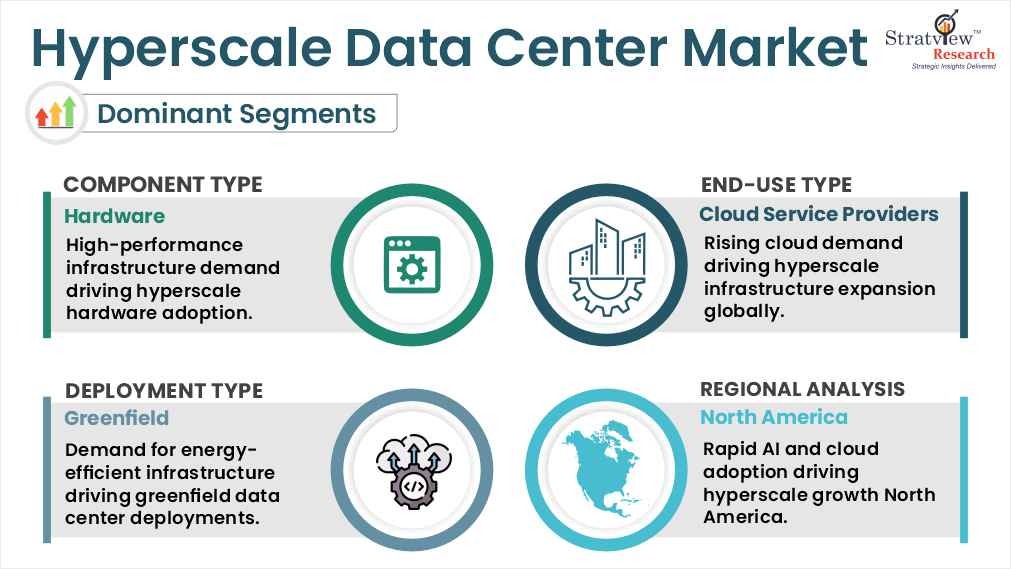

Hardware segment is projected to be the dominant segment during the forecast period. |

|

Deployment Type Analysis |

Greenfield & Brownfield |

Greenfield segment is expected to be the dominant segment during the forecast period. |

|

Power Capacity Type Analysis |

10-50 MW, 50-100 MW, and Above 101 MW |

10-50 MW segment is expected to be the fastest-growing segment during the forecast period. |

|

End Use Type Analysis |

Cloud Service Providers, Colocation Service Providers, and Enterprises |

Cloud Service Providers segment is expected to be the dominant segment during the forecast period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to be the dominant and fastest-growing region over the forecasted period. |

“Hardware segment is projected to be the dominant segment during the forecast period.”

“Cloud service provider segment is projected to be the dominant segment during the forecast period.”

“Greenfield segment is projected to be the dominant segment during the forecast period.”

Want to get more details about the segmentations? Register Here

“North America is expected to be the dominant and fastest-growing region over the forecasted period.”

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the hyperscale data center market -

Note: The above list does not necessarily include all the top players in the market.

Are you a leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

|

Market Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2032 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

5 (Component Type, Deployment Type, Power Capacity Type, End-use Type and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

This report studies the market, covering a period of 15 years of trend and forecast. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The hyperscale data center market is segmented into the following categories:

By Component

By Deployment Type

By Power Capacity Type

By End-Use Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The hyperscale data center market refers to the industry focused on large-scale data center facilities designed to efficiently support massive volumes of data processing, storage, and networking. Usually run by large cloud service providers and IT firms, these data centers are designed to provide high performance, scalability, and dependability. Advanced technologies, including cloud computing, big data analytics, machine learning, and artificial intelligence (AI) are powered in large part by hyperscale facilities. The market includes the software, services, and infrastructure elements that make it possible for these expansive settings to function and grow across different sectors and geographical areas.

The forecasted value for the market is US$ 957.53 billion in 2032.

Hyperscale data center market size was USD 162.2 billion in 2024 and is expected to grow from USD 203.07 billion in 2025 to USD 957.53 billion in 2032, witnessing an impressive market growth (CAGR) of 24.80% during the forecast period (2025-2032).

The key drivers of the hyperscale data center market include rising industrial automation, adoption of AI and ML and expansion of 5G Infrastructure.

The top players in the hyperscale data center market include • ABB (US) • Alibaba (China) • Arista Networks (US) • AWS (US) • Cisco (US) • Dell (US) • Google (US) • HPE (US) • IBM (US) • Microsoft (US) • NVIDIA (US) • Nlyte Software (US) • Oracle (US) • Quanta Cloud Technology (US) • Tencent (China) • Vertiv (US)

North America is expected to be the dominant and the fastest-growing region of the hyperscale data center market over the forecasted period, driven by robust digital infrastructure, advanced technological adoption, and growing demand for cloud services.

WE ACCEPT