404

+1-313-307-4176

Aircraft Pumps Market | 2025-2034

Aircraft Pumps Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2025-2034

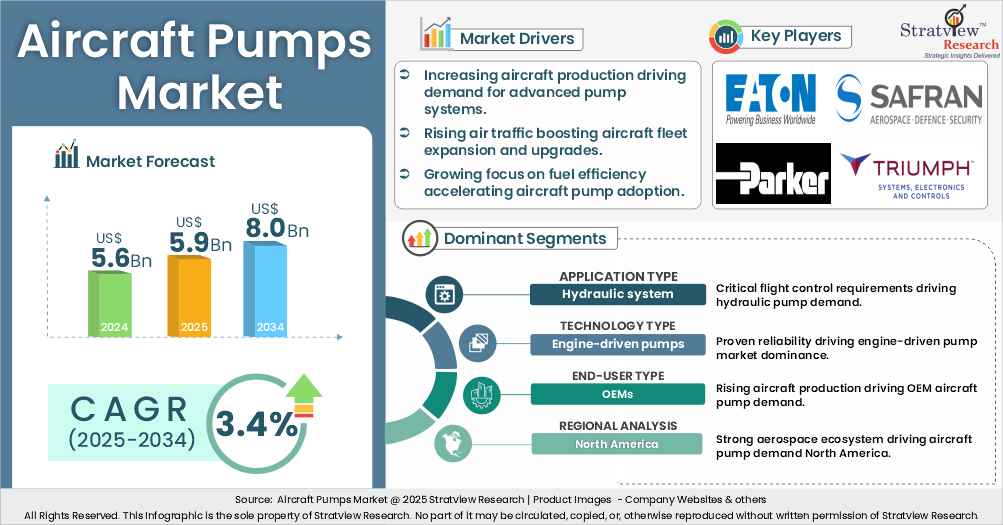

"Aircraft pumps market size was USD 5.6 billion in 2024.”

The market size in 2023 was USD 5.0 billion. In 2024, the market experienced a YoY growth of 10.9% to reach a value of USD 5.6 billion.

The market is expected to reach USD 5.9 billion in 2025, witnessing an annual growth of 6.2%.

The market size will reach USD 8.0 billion in 2034, witnessing a market growth (CAGR) of 3.4% during the forecast period of 2025-2034.

The annual demand for aircraft pumps was USD 5.6 billion in 2024 and is expected to reach USD 5.9 billion in 2025, up 6.2% than the value in 2024.

During the forecast period (2025-2034), the aircraft pumps market is expected to grow at a CAGR of 3.4%. The annual demand will reach USD 8.0 billion in 2034.

During 2025-2034, the aircraft pumps industry is expected to generate a cumulative sales opportunity of USD 71.9 billion, which is almost 2.5 times the opportunities during 2019-2024.

Want to get a free sample? Register Here

North America is expected to maintain its reign over the forecast period, whereas Asia-Pacific is likely to grow at the fastest rate.

By aircraft type, Commercial aircraft are expected to be the biggest demand generator for pumps in the market and are likely to grow at the fastest rate in the coming years.

By pump type, Hydraulic pumps are anticipated to contribute the largest share of the aircraft pumps market during the forecast period.

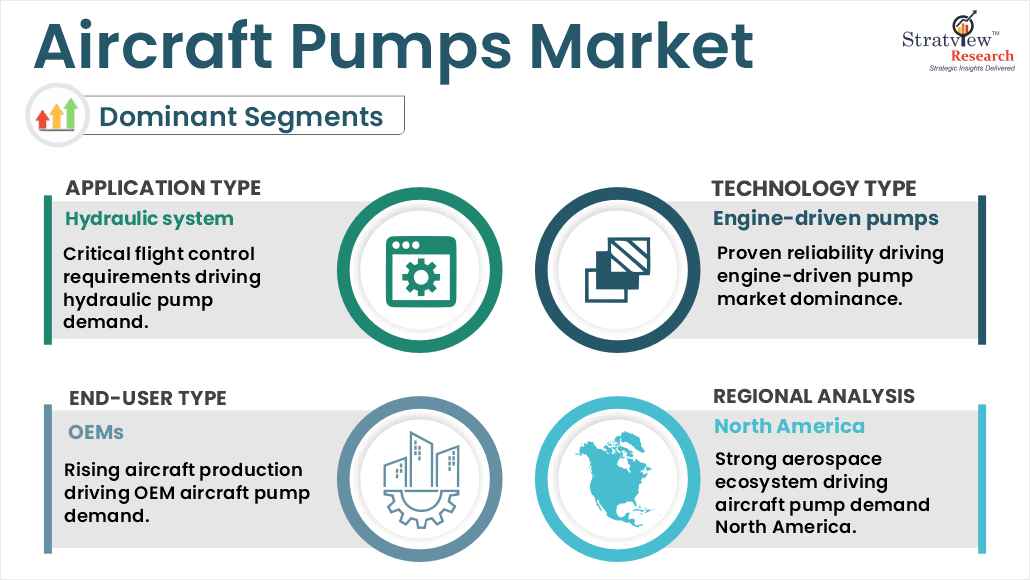

By application type, Hydraulic system is expected to be the dominant application type in the aircraft pumps market during the study period.

By technology type, Engine-driven pumps are likely to hold the major share of the aircraft pumps market.

By category type, Positive displacement pumps are projected to maintain their unconquerable lead throughout the study period.

By end-user type, OEM is anticipated to remain the pioneer in the market throughout the study period.

Have a look at the sales opportunities presented by the aircraft pumps market in terms of growth and market forecast.

|

Aircraft Pumps Market Data & Statistics |

|

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

|

Annual Market Size in 2023 |

USD 5.0 billion |

- |

|

|

Annual Market Size in 2024 |

USD 5.6 billion |

YoY Growth in 2024: 10.9% |

|

|

Annual Market Size in 2025 |

USD 5.9 billion |

YoY Growth in 2025: 6.2% |

|

|

Annual Market Size in 2034 |

USD 8.0 billion |

CAGR 2025-2034: 3.4% |

|

|

Cumulative Sales Opportunity during 2025-2034 |

USD 71.9 billion |

- |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 4.5 billion + |

> 80% |

|

|

Top 10 Company’s Market Share in 2024 |

USD 2.8 billion to USD 3.9 billion |

50% - 70% |

|

Rising Global Aircraft Production and Fleet Expansion

Growing commercial and military aircraft production, coupled with long-term fleet expansion and modernization programs, is driving aircraft pumps market growth by increasing demand for hydraulic, fuel, lubrication, and cooling pumps. Aircraft pumps are essential for flight safety, engine performance, and fuel management, supporting both line-fit installations in new aircraft and replacement demand across the global fleet.

According to the International Air Transport Association (IATA) the global commercial aircraft fleet comprised approximately 35,550 aircraft as of June 2025, including 30,300 active aircraft, highlighting the expanding installed base that drives sustained demand for aircraft pump systems.

According to the International Civil Aviation Organization (ICAO) ), its Long-Term Forecast platform provides aircraft fleet, traffic, and personnel forecasts for up to 30 years across global markets, reflecting sustained long-term growth in aircraft fleets and supporting continued demand for aircraft systems such as hydraulic, fuel, lubrication, and cooling pumps.

Strong Aircraft Order Backlogs and Rising Air Passenger Traffic

Strong aircraft order backlogs and continued growth in global air passenger traffic are driving aircraft pumps market demand by increasing long-term procurement of aircraft systems. New-generation aircraft require advanced fuel, hydraulic, and thermal management systems, creating sustained demand from OEMs and tier suppliers across the aviation value chain.

According to Airbus' Global Market Forecast 2025–2044, demand for approximately 43,400 new passenger and freighter aircraft is expected over the next 20 years, driven by rising passenger traffic and fleet replacement, strengthening long-term aircraft pumps market demand.

According to the U.S. Federal Aviation Administration (FAA), U.S. airlines carried approximately 862.8 million system revenue passengers in 2024, up 5.0% from 2023, reflecting sustained growth in air travel that supports aircraft pumps market demand through increased aircraft procurement and aftermarket activities.

Persistent Aerospace Supply Chain Disruptions

Persistent aerospace supply chain disruptions continue to affect aircraft production schedules and component availability. Pump manufacturers face delays in raw materials, castings, electronics, and specialized aerospace-grade components, resulting in longer lead times and production inefficiencies across the supply network.

Stringent Certification and Regulatory Compliance Requirements

Aircraft pumps must comply with stringent aviation safety, certification, and reliability requirements. The extensive qualification and approval process increases development costs and extends product commercialization timelines, particularly for suppliers introducing advanced electric or lightweight pump technologies.

According to the International Civil Aviation Organization (ICAO), its 193 Member States are required to implement Standards and Recommended Practices (SARPs) across 19 Annexes to the Convention on International Civil Aviation, covering areas such as airworthiness, aircraft operations, and safety management. Compliance with these stringent global aviation standards increases certification complexity, development costs, and time-to-market for aircraft pump manufacturers.

Fleet Modernization and Next-Generation Aircraft Programs

Fleet modernization and next-generation aircraft programs are accelerating the adoption of more efficient and electrically driven systems. Advanced fuel, hydraulic, and cooling pumps designed for reduced weight, improved energy efficiency, and predictive maintenance capabilities are expected to gain wider acceptance, strengthening the aircraft pumps market forecast over the coming years.

According to Boeing's Commercial Market Outlook 2025–2044, the global commercial aircraft fleet is projected to grow to approximately 49,600 aircraft by 2044, with demand for 43,600 new airplanes, of which about 21,000 deliveries will replace older aircraft. This fleet renewal trend is expected to create significant opportunities for advanced aircraft pump technologies designed for next-generation platforms.

| Segmentations | List of Sub-Segments | Segments with High-Growth Opportunity |

|

Aircraft-Type Analysis |

Commercial Aircraft, Military Aircraft, Regional Aircraft, Business Jet, and Helicopter |

Commercial aircraft are expected to be the biggest demand generator for pumps in the market and are likely to grow at the fastest rate in the coming years. |

|

Pump-Type Analysis |

Fuel Pumps, Hydraulic Pumps, Lube & Scavenge Pumps, Water & Wastewater Pumps, and Air Conditioning & Cooling Pumps |

Hydraulic pumps are anticipated to contribute the largest share of the aircraft pumps market during the forecast period. |

|

Application-Type Analysis |

Hydraulic System, Engine, Auxiliary & Emergency Applications, Gearbox, Onboard Lavatory System, and ECS |

Hydraulic system is expected to be the dominant application type in the aircraft pumps market during the study period. |

|

Technology-Type Analysis |

Engine-Driven Pumps, Electric Motor-Driven Pumps, and Others |

Engine-driven pumps are likely to hold the major share of the aircraft pumps market. |

|

Category-Type Analysis |

Positive Displacement Pumps and Nonpositive Displacement Pumps |

Positive displacement pumps are projected to maintain their unconquerable lead throughout the study period. |

|

End-User-Type Analysis |

OEM and Aftermarket |

OEM is anticipated to remain the pioneer in the market throughout the study period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to maintain its reign over the forecast period, whereas Asia-Pacific is likely to grow at the fastest rate. |

“Commercial aircraft are expected to maintain their dominance by registering the highest growth in the market during the forecast period.”

The aircraft pumps market is segmented into commercial aircraft, military aircraft, regional aircraft, business jets, and helicopters.

Commercial aircraft are expected to remain dominant as well as the fastest-growing aircraft type in the market during the forecast period. Commercial aircraft dominate the aircraft pumps market due to their large-scale operations, high production rates, and continuous demand for maintenance and upgrades. These aircraft require various pumps for essential functions such as fuel delivery, hydraulic control, lubrication, and cooling systems. As global air travel grows, airlines are expanding and modernizing their fleets, driving consistent demand for both new and replacement pump systems.

One of the biggest reasons for this dominance is the sheer volume of commercial aircraft in operation worldwide. Major manufacturers like Boeing and Airbus deliver hundreds of jets annually, each equipped with multiple pump systems. Unlike military procurement, which is periodic and budget-dependent, commercial aviation sees steady, predictable growth based on passenger traffic and airline profitability.

Additionally, commercial aircraft have long service lives, often 20 years or more, which leads to sustained demand for maintenance, repair, and overhaul (MRO) services. Pumps are among the critical components that require regular service to ensure flight safety and system reliability, making the aftermarket a major revenue driver in the commercial category. The shift toward more electric aircraft (MEA) is also accelerating pump innovation in commercial aviation. With a global network of airlines, high utilization rates, and constant technological upgrades, commercial aviation represents the most dynamic and profitable segment of the aircraft pumps market, ensuring its continued dominance in the years ahead.

“Hydraulic pumps are likely to remain the most demanding pump type in the aircraft pumps market.”

The market is segmented into fuel pumps, hydraulic pumps, lube & scavenge pumps, water & wastewater pumps, and air conditioning & cooling pumps.

Hydraulic pumps are the dominant and fastest-growing pump type in the aircraft pumps market due to their critical role in essential flight control systems and aircraft operations. These pumps are responsible for powering a wide range of high-force applications, including landing gear systems, flight control surfaces (such as flaps, slats, and rudders), brakes, and thrust reversers. Their ability to deliver high power density in a compact and reliable form makes them indispensable in both commercial and military aircraft.

Moreover, as aircraft continue to become more advanced, the demand for efficient and robust hydraulic systems has only increased. Even with the shift toward more electric aircraft (MEA), many large and long-haul aircraft still rely heavily on hydraulic systems due to their proven reliability and capability in high-load, high-pressure applications. This has helped sustain demand for hydraulic pumps across both new aircraft production and the aftermarket.

Additionally, the retrofitting and maintenance of aging aircraft fleets, particularly in regions like North America and Europe, contributes to the continued need for hydraulic pump replacements and upgrades. These factors, combined with the broad application of hydraulic systems across various aircraft types and the slow transition to fully electric systems, reinforce the dominance of hydraulic pumps in the aircraft pumps market.

“Hydraulic system is likely to remain the dominant application type in the aircraft pumps market during the forecast period.”

The market is segmented into hydraulic system, engine, auxiliary & emergency applications, gearbox, onboard lavatory system, and ECS.

Hydraulic system applications are dominant in the aircraft pumps market because they are essential for controlling critical aircraft functions that require high power, precision, and reliability. From operating landing gear and flight control surfaces to actuating brakes and thrust reversers, hydraulic systems are central to the safe and efficient operation of virtually all types of aircraft. These systems rely heavily on pumps to generate the necessary pressure, making them the largest application area for aircraft pumps.

One of the biggest reasons for their dominance is their versatility and high force output. Hydraulic systems can handle intense mechanical loads while maintaining precise control, making them indispensable in both commercial and military aircraft. As aircraft designs evolve, the need for reliable, compact, and efficient hydraulic actuation continues to grow, reinforcing the importance of pumps in these systems.

At the same time, gearbox applications are emerging as the fastest-growing category, driven by the increasing complexity and performance demands of modern engines and propulsion systems. Gearboxes require dedicated pumps to provide lubrication, cooling, and pressure regulation, ensuring optimal performance and durability of rotating components under extreme conditions. The rapid growth in fuel-efficient engines, geared turbofan technology, and electric hybrid propulsion systems has accelerated the need for high-performance pumps for gearboxes. With hydraulic systems serving as the backbone of traditional flight control and aircraft operation, and gearboxes powering the next generation of propulsion technologies, these two application areas are defining the current and future landscape of the aircraft pumps market.

“Engine-driven pumps rule the aircraft pumps market, whereas electric motor-driven pumps are likely to witness the highest growth during the forecast period.”

The market is segmented into engine-driven pumps, electric motor-driven pumps, and others. Engine-driven pumps are dominant in the aircraft pumps market due to their high reliability, strong power output, and deep integration with conventional aircraft engines. These pumps are mechanically powered by the aircraft's engine and operate continuously during flight, supplying essential hydraulic or fuel pressure to core systems such as flight controls, landing gear, and braking mechanisms. Their consistent performance and ability to function under high loads make them the preferred choice in most commercial and military aircraft.

One of the biggest reasons for their dominance is their established track record in traditional aircraft architecture. Engine-driven pumps are durable, capable of withstanding harsh operational environments, and require minimal electronic control, which adds to their simplicity and dependability. Their continuous operation ensures critical systems remain active throughout all flight phases, especially in long-haul and high-performance aircraft.

In contrast, electric motor-driven pumps are the fastest-growing technology type, driven by industry’s shift toward More Electric Aircraft (MEA). These pumps offer on-demand operation, allowing systems to activate only when needed, which reduces energy consumption and improves overall efficiency. Unlike engine-driven pumps, electric pumps are not tied to engine operation, providing greater flexibility in system design and operation.

Want to get more details about the segmentations? Register Here

“OEMs are expected to remain the dominant and faster-growing end-user of the market during the forecast period.”

The market is segmented into OEM and aftermarket. Original Equipment Manufacturers (OEMs) are expected to remain both the dominant and fastest-growing end-users in the aircraft pumps market during the forecast period due to several key factors. Firstly, the global rise in aircraft production, driven by increasing air travel demand, fleet modernization efforts, and the introduction of more fuel-efficient aircraft is fueling OEM demand for advanced components, including pumps. As aircraft manufacturers like Boeing, Airbus, and emerging regional players ramp up production to meet growing backlogs, the requirement for pumps as integral components in new aircraft builds continues to surge.

Additionally, OEMs are at the forefront of adopting new technologies in line with the More Electric Aircraft (MEA) trend and sustainable aviation goals. This positions them as key consumers of innovative pump systems, such as electric motor-driven pumps and integrated modular solutions, to improve energy efficiency and reduce emissions.

The combination of rising aircraft production, technological innovation, and the push for electrification ensures that OEMs not only maintain their dominance but also experience the fastest growth in the aircraft pumps market during the forecast period.

“North America is likely to hold the lion’s share of the aircraft pumps market throughout the study period, whereas Asia-Pacific is expected to grow at a faster pace during the same period.”

North America is the dominant region in the aircraft pumps market due to its well-established aerospace industry, presence of major aircraft OEMs, and strong military aviation capabilities. Home to global aerospace leaders like Boeing, Lockheed Martin, and Raytheon Technologies, the region has a highly developed ecosystem for aircraft production, innovation, and defense operations. These companies consistently generate high demand for advanced pump systems across both commercial and military aircraft platforms.

One of the biggest reasons for North America’s dominance is its large fleet of in-service aircraft and steady production output, particularly in the United States. The region also benefits from substantial defense spending, which fuels continuous development and procurement of fighter jets, transport aircraft, and other military platforms requiring high-performance pumps. Additionally, a mature MRO (Maintenance, Repair, and Overhaul) infrastructure supports aftermarket demand, further reinforcing North America’s leading position in the market.

In contrast, Asia-Pacific is the fastest-growing region, driven by rapid air traffic growth, expanding commercial airline fleets, and increasing defense investments. Countries like China, India, Japan, and South Korea are heavily investing in both civil and military aviation, leading to rising aircraft production and modernization programs that demand new-generation pump systems. Asia-Pacific's commercial aviation industry is experiencing a surge in passenger traffic, prompting major airlines to place large aircraft orders and expand routes across the region.

Most of the major players compete in some of the factors, including price, service offerings, regional presence, etc. The following are the key players in the aircraft pumps market -

Here is the list of the Top Players (Based on Dominance)

Eaton Corporation plc

Parker Hannifin Corporation

Safran S.A.

Triumph Group

Crane Aerospace & Electronics

Liebherr Group

Woodward Inc.

RTX Corporation

Honeywell International Inc.

ESCO Technologies Inc. (Crissair Inc.)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Service portfolio, New Product Launches, etc.

COVID-19 impact and its recovery curve.

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

|

Market Study Period |

2019-2034 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2034 |

|

Trend Period |

2019-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

7 (Aircraft Type, Pump Type, Application Type, Technology Type, Category Type, End-User Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aircraft pumps market is segmented into the following categories:

Aircraft Pumps Market, by Aircraft Type

Commercial Aircraft

Military Aircraft

Regional Aircraft

Business Jet

Helicopter

Aircraft Pumps Market, by Pump Type

Fuel Pumps

Hydraulic Pumps

Lube & Scaenge Pumps

Water & Wastewater Pumps

Air Conditioning & Cooling Pumps

Aircraft Pumps Market, by Application Type

Hydraulic System

Engine

Auxiliary & Emergency Applications

Gearbox

Onboard Lavatory System

ECS

Aircraft Pumps Market, by Technology Type

Engine-Driven Pumps

Electric Motor-Driven Pumps

Others

Aircraft Pumps Market, by Category Type

Positive Displacement Pumps (Regional Analysis and Sub-Category Analysis)

Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World

Sub-Category Analysis: Fixed Displacement Pumps and Variable Displacement Pumps

Nonpositive Displacement Pumps (Regional Analysis and Sub-Category Analysis)

Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World

Sub-Category Analysis: Centrifugal Pump and Others

Aircraft Pumps Market, by End-User Type

OE

Aftermarket

Aircraft Pumps Market, by Region

North America (Country Analysis: The USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, The UK, Russia, and the Rest of Europe)

Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others)

This strategic assessment report from Stratview Research provides a comprehensive analysis that reflects today’s aircraft pumps market realities and future market possibilities for the forecast period.

The report segments and analyzes the market in the most detailed manner to provide a panoramic view of the market.

The vital data/information provided in the report can play a crucial role for market participants and investors in identifying the low-hanging fruits available in the market and formulating growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools.

More than 1,000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data.

We conducted more than 15 detailed primary interviews with market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respectable clients:

Company Profiling

Detailed profiling of additional market players (up to three players)

SWOT analysis of key players (up to three players)

Competitive Benchmarking

Benchmarking of key players on the following parameters: Service portfolio, geographical reach, regional presence, and strategic alliances

Custom Research: Stratview Research offers custom research services across sectors. In case of any custom research requirement related to Market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

An aircraft pump is a device used in airplanes to move fluids like fuel, hydraulic oil, or lubricants through different systems. These pumps help operate important functions such as raising and lowering the landing gear, controlling the brakes, powering flight controls, and supplying fuel to the engines. They can be powered by the engine, electricity, or used as backups in emergencies. Aircraft pumps are designed to be reliable, lightweight, and strong enough to work in tough conditions like high altitudes and extreme temperatures.

The aircraft pumps market is estimated to grow at a CAGR of 3.4% to reach an annual market size of US$ 8.0 billion by 2034, driven by recovery in air passenger traffic, rising aircraft fleet size, increasing military expenditure, and aging aircraft fleet size.

Electric motor-driven pump technology is expected to offer high-growth opportunities in the aircraft pumps market over the long term, primarily due to the aviation industry's shift toward More Electric Aircraft (MEA), which favors electric over mechanical systems for improved efficiency and weight reduction. These pumps support on-demand operation, enhancing fuel efficiency and aiding in carbon emission reduction—key priorities for modern aircraft. Additionally, their compatibility with hybrid and electric propulsion systems, lower maintenance needs, higher reliability, and greater flexibility in system design make them ideal for next-generation aircraft.

Eaton Corporation, Parker Hannifin Corporation, Safran S.A., Triumph Group, Crane Aerospace & Electronics, and Liebherr Group are the leading players in the aircraft pumps market.

North America holds the largest market share in the aircraft pumps market due to the presence of major aircraft manufacturers like Boeing and Raytheon Technologies, along with high demand from both the military and commercial aviation industry. The region benefits from significant defense spending, a large commercial aviation fleet, and strong investments in research and development, particularly in the advancement of electric and hybrid-electric aircraft technologies. Additionally, North America's well-established aerospace supply chain and infrastructure further support its dominance in the market.

Asia-Pacific region is projected to be the fastest-growing in the aircraft pumps market during the forecast period. This growth is driven by rapid economic development, increasing air travel demand, and significant investments in aerospace infrastructure in countries like China and India. These nations are emerging as key aviation hubs, with expanding fleets and modernizing airports, which in turn drives the need for advanced aircraft components, including pumps.

Hydraulic systems are crucial for the operation of several key components in aircraft, including flight controls, landing gear, brakes, and thrust reversers. These systems require reliable and high-power pumps to operate efficiently under high pressure and demanding conditions, making hydraulic pumps essential in both commercial and military aviation. Despite the increasing adoption of electric systems, hydraulic systems remain dominant due to their proven performance and ability to handle high-load applications, especially in legacy and current aircraft models. As such, the hydraulic systems segment continues to hold the largest share in the aircraft pumps market.

WE ACCEPT