404

+1-313-307-4176

Antifreeze Market Analysis | 2024-2032

Antifreeze Market Size, Share, Trends, Dynamics, Forecast, & Growth Analysis: 2024-2032

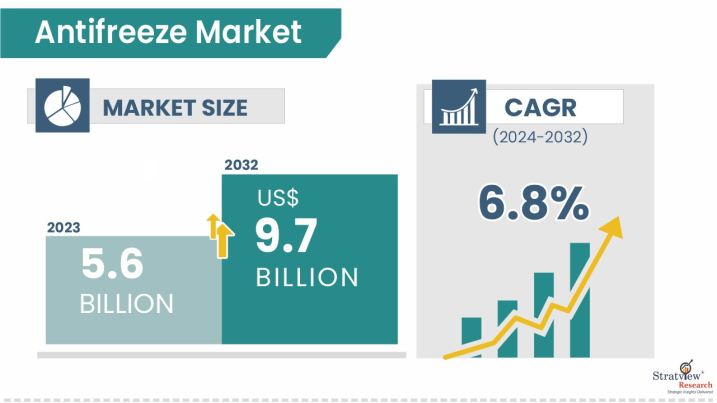

The antifreeze market size was USD 5.6 billion in 2023 and is likely to grow at a robust CAGR of 6.8% during 2024-2032 to reach USD 9.7 billion in 2032.

Want to know more about the market scope? Register Here

Antifreeze, also known as engine coolant, represents a critical fluid additive designed to regulate engine temperature by preventing freezing in cold conditions and boiling in high-temperature environments. These specialized chemical formulations combine water with various glycol-based compounds, corrosion inhibitors, and performance additives to maintain optimal thermal management across diverse operating conditions. The market encompasses multiple formulation types, from traditional ethylene glycol-based solutions to environmentally friendly propylene glycol alternatives, serving automotive, industrial, and specialized application sectors worldwide.

Modern antifreeze formulations have evolved significantly beyond basic freeze protection, incorporating advanced additive packages that provide extended service life, enhanced corrosion protection, and compatibility with contemporary materials, including aluminum, plastic, and rubber components. This evolution reflects the industry's response to increasingly sophisticated engine designs, stringent environmental regulations, and demand for longer service intervals that reduce maintenance costs and environmental impact.

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Product-Type Analysis |

Ethylene Glycol, Propylene Glycol, Glycerin, and Others. |

Ethylene glycol-based antifreeze is expected to remain dominant, whereas propylene glycol-based formulations will be the fastest-growing product type in the market during the forecast period. |

|

Application-Type Analysis |

Automotive, Aerospace, Industrial, Construction, Electronics, and Others |

Automotive applications are expected to remain the dominant and fastest-growing application segment in the market during the forecast period. |

|

Technology-Type Analysis |

Organic Acid Technology (OAT), Inorganic Acid Technology (IAT), Hybrid Organic Acid Technology (HOAT), and Others |

Organic Acid Technology (OAT) is expected to remain dominant, whereas Hybrid Organic Acid Technology (HOAT) will be the fastest-growing technology type in the market during the forecast period. |

|

Distribution-Channel-Type Analysis |

OEM, Aftermarket, and Others |

OEM channels are expected to remain dominant, whereas aftermarket distribution will be the fastest-growing channel type in the market during the forecast period. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

Asia-Pacific is expected to remain the largest market for global antifreeze during the forecast period. |

“Ethylene glycol-based antifreeze is expected to remain dominant, whereas propylene glycol-based formulations will be the fastest-growing product type in the market during the forecast period.”

Ethylene glycol-based, propylene glycol-based, glycerin-based, and other specialty formulations make up the worldwide antifreeze industry. Propylene glycol-based substitutes will rise at the fastest rate over the projected period, while ethylene glycol-based goods are anticipated to continue dominating the market.

Because of its excellent heat transfer qualities, affordability, and broad OEM approval among automakers, ethylene glycol-based antifreeze continues to rule the market. When combined in 50/50 ratios with water, these compositions offer exceptional freeze protection down to -34°F (-37°C), and their outstanding thermal conductivity allows for effective engine cooling. However, alternate formulations are becoming more popular due to toxicity concerns and environmental constraints.

The fastest-growing category is propylene glycol-based antifreeze, which is fueled by decreased toxicity, environmental safety, and food-grade certification that allows for a wider range of applications.

“Automotive applications are expected to remain the dominant and fastest-growing application segment of the market during the forecast period.”

Automotive, aerospace, industrial, construction, electronics, and other specialized applications make up the market segments. Over the course of the projection period, automotive applications are anticipated to continue to be the market's leading category while also seeing strong growth.

The dominance of the automotive industry is a result of ongoing worldwide vehicle production expansion, especially in emerging nations where growing middle-class populations encourage the purchase of new cars. Growing automobile production worldwide, especially in nations like China, Brazil, and India, helps the market by generating steady demand for both OEM fill and aftermarket replacement coolants. Additionally, since aging cooling systems need more regular maintenance, rising average vehicle ages in developed markets fuel aftermarket demand.

Due to the need for precise heat management in manufacturing processes, data centers, and growing HVAC systems, industrial applications provide substantial growth potential.

“Organic Acid Technology (OAT) is expected to remain dominant, whereas Hybrid Organic Acid Technology (HOAT) will be the fastest-growing technology type of the market during the forecast period.”

Organic Acid Technology (OAT), Inorganic Additive Technology (IAT), Hybrid Organic Acid Technology (HOAT), and other specialist formulations comprise the worldwide antifreeze market. It is anticipated that OAT-based antifreeze will continue to dominate the market, while HOAT formulations will increase at the quickest rate throughout the course of the projection period.

The improved extended-life performance of Organic Acid Technology, which offers service intervals up to 150,000 miles or five years instead of the customary 30,000-mile intervals, is the reason for its domination. Organic carboxylate inhibitors, which are used in OAT formulations, offer superior long-term corrosion protection for aluminum and other contemporary engine materials without creating silicate deposits that could lower heat transfer efficiency. Widespread commercial acceptability has been fueled by the adoption of OAT as the preferred coolant technology by major automakers such as General Motors, Volkswagen, and Asian manufacturers.

“OEM channels are expected to remain dominant, whereas aftermarket distribution will be the fastest-growing channel type of the market during the forecast period.”

The market is divided into three segments: direct sales channels, aftermarket, and OEM (Original Equipment Manufacturer). Over the course of the forecast period, aftermarket channels are anticipated to develop at the fastest rate, while OEM distribution is predicted to continue to be the most important channel.

Because factory-fill coolant is necessary for every new car, OEM channel dominance results in a guaranteed baseline demand that is directly correlated with worldwide vehicle production levels. OEM alliances give antifreeze producers stable, long-term contracts, chances for technical cooperation, and formulation quality validation that improves brand reputation. Established suppliers with demonstrated technical capability are favored by competitive barriers created by major automakers' strict qualifying standards.

The fastest-growing channel is aftermarket distribution, which is fueled by growing independent service center networks, an aging global vehicle fleet, and rising consumer awareness of maintenance needs.

“Asia-Pacific is expected to remain the largest market for antifreeze during the forecast period.”

Over the course of the forecast period, Asia-Pacific is anticipated to continue to hold the top spot in the regional antifreeze market. At 42.3%, the Asia-Pacific (APAC) region has the largest proportion due to its enormous automobile production capacity, quickly growing industrial sectors, and rising consumer car ownership in major economies like China, India, Japan, and South Korea.

OEM antifreeze is in high demand due to China's supremacy in automotive production, which produces more than 25 million cars a year. Significant growth prospects are created by India's growing automobile industry and rising car penetration rates in both rural and urban markets. Advanced automotive technologies and premium car segments that call for specific coolant formulas are two ways in which South Korea and Japan contribute.

Know the high-growth countries in this report. Register Here

The market is highly fragmented, with over 200 players. Most of the major players compete in some of the governing factors, including price, service offerings, and regional presence etc. The following are the key players in the antifreeze market. Some of the major players provide a complete range of services.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The antifreeze market is segmented into the following categories.

By Product Type

By Application Type

By Technology Type

By Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected].

To prevent freezing in cold weather and to provide boiling point elevation, corrosion prevention, and optimal heat transfer in automotive and industrial cooling systems, antifreeze is a specialized chemical ingredient that is mixed with water to form engine coolant.

The forecasted value of the antifreeze market is expected to be USD 9.7 billion in 2032.

By 2032, the global antifreeze market is expected to increase at a compound annual growth rate (CAGR) of 6.8% due to factors such as rising vehicle production worldwide, expanding industrial uses, rising aftermarket demand, and technological breakthroughs in coolant formulations.

Stricter environmental regulations encouraging safer formulations, growing adoption of electric vehicles necessitating specialized thermal management solutions, expanding data center and electronics cooling applications, growing global automotive production, and an aging vehicle fleet requiring aftermarket service are some of the major drivers.

Propylene glycol-based solutions for environmental safety, electronics applications spurred by data center expansion, electric vehicle coolants for battery thermal management, and extended-life formulations lowering maintenance frequency are examples of high-growth categories.

Due to China's enormous automobile production capacity, India's growing car ownership, and the region's strong industrial growth, the Asia-Pacific region has the greatest market share, at roughly 42.3%.

Due to strict environmental laws, aggressive goals for the adoption of electric vehicles, and industrial decarbonization programs that support cutting-edge coolant technology, Europe is predicted to develop at the fastest rate in the region.

Exxon Mobil Corporation, BASF SE, Royal Dutch Shell PLC, Chevron Corporation, Total Energies SE, BP Plc, Valvoline Inc., Motul S.A., Prestone Products Corporation, and Old-World Industries LLC are the leading players in the global antifreeze market.

WE ACCEPT