404

+1-313-307-4176

Data Center Liquid Cooling Market | 2025-2031

Data Center Liquid Cooling Market Size, Share, Trend, Forecast, Competitive Landscape & Growth Opportunities: 2025-2031

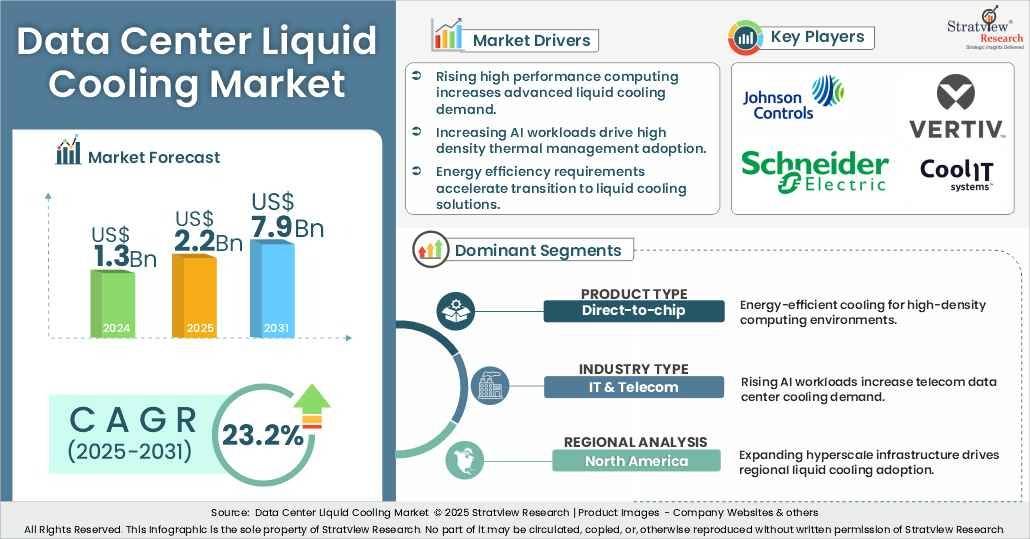

"Data center liquid cooling market size was USD 1.3 billion in 2024.”

The market size in 2023 was USD 0.8 billion. In 2024, the market experienced a YoY growth of 72.4% to reach a value of USD 1.3 billion.

The market is expected to reach USD 2.2 billion in 2025, witnessing an annual growth of 68.2%.

The market size will reach USD 7.9 billion in 2031, witnessing a market growth (CAGR) of 23.2% during the forecast period of 2025-2031.

The annual demand for data center liquid cooling was USD 1.3 billion in 2024 and is expected to reach USD 2.2 billion in 2025, up 68.2% than the value in 2024.

During the forecast period (2025-2031), the data center liquid cooling market is expected to grow at a CAGR of 23.2%. The annual demand will reach USD 7.9 billion in 2031, which is almost 3.5 times the demand in 2025.

During 2025-2031, the data center liquid cooling industry is expected to generate a cumulative sales opportunity of USD 35.1 billion.

Want to get a free sample? Register Here

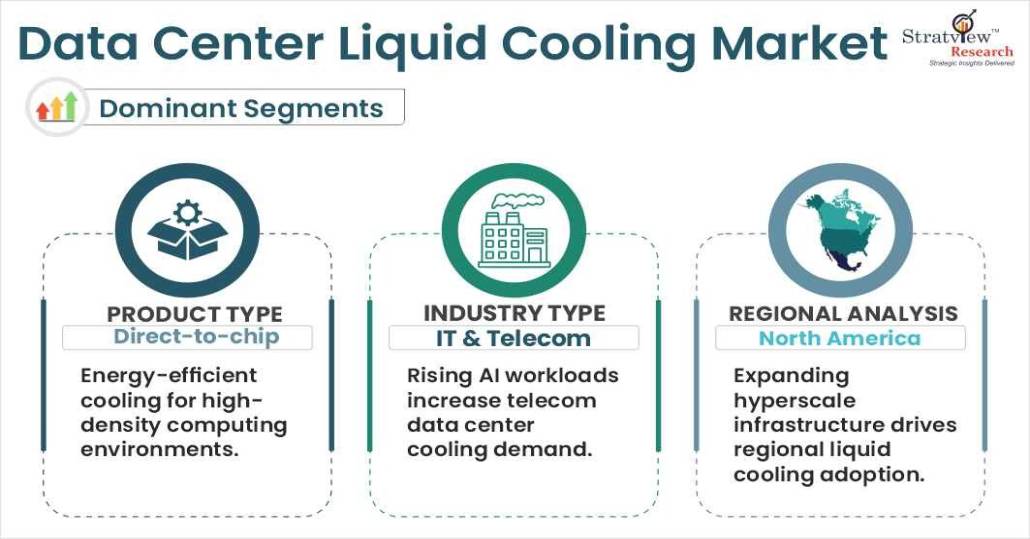

North America is expected to remain the largest market, whereas Asia-Pacific is likely to be the fastest-growing market during the forecast period.

By product type, the direct-to-chip segment holds the largest market share and is projected to experience the fastest growth in the coming years.

By end-use industry type, IT & Telecom is expected to be the leading category of the market, whereas BFSI is expected to grow at the fastest pace.

Have a look at the sales opportunities presented by the data center liquid cooling market in terms of growth and market forecast.

|

Data Center Liquid Cooling Market Data & Statistics |

|

||

|

Market Statistics |

Value (in USD Billion) |

Market Growth (%) |

|

|

Annual Market Size in 2023 |

USD 0.8 billion |

- |

|

|

Annual Market Size in 2024 |

USD 1.3 billion |

YoY Growth in 2024: 72.4% |

|

|

Annual Market Size in 2025 |

USD 2.2 billion |

YoY Growth in 2025: 68.2% |

|

|

Annual Market Size in 2031 |

USD 7.9 billion |

CAGR 2025-2031: 23.2% |

|

|

Cumulative Sales Opportunity during 2025-2031 |

USD 35.1 billion |

- |

|

|

Top 10 Countries’ Market Share in 2024 |

USD 1 billion + |

> 80% |

|

|

Top 10 Company’s Market Share in 2024 |

USD 0.6 billion to USD 0.9 billion |

50% - 70% |

|

Want to get a free sample? Register Here

Data center liquid cooling is an advanced thermal-management technology that uses liquid (typically water or engineered dielectric fluids) to absorb and transfer heat directly from high-power IT components such as CPUs, GPUs, and high-density racks. By enabling more efficient heat removal than air cooling, it supports higher compute densities, improved energy efficiency, and lower operating costs. Modern deployments typically include direct-to-chip and immersion architectures with integrated cold plates, CDUs, and heat exchangers

Rising Rack Power Density Driven by AI and HPC

The surge in computational demand is becoming a major driver for liquid-cooling adoption in data centers. Rack densities that once averaged around 15 kW are now climbing to 80–120 kW in AI environments, surpassing what conventional air-cooling can effectively manage.

For example, joint initiatives by Schneider Electric and NVIDIA are enabling AI facilities engineered to handle up to 132 kW per rack with liquid-cooling designs. This growing thermal intensity is driving operators to invest more in liquid cooling to ensure efficiency, uptime, and optimal system performance.

Energy Efficiency Benefits

Energy efficiency is a key factor accelerating adoption in the liquid cooling market. Studies indicate that fully implemented liquid-cooling systems can reduce facility power consumption by about 18.1% and overall data center energy use by roughly 10.2% compared with conventional air-cooling approaches.

These measurable savings help operators lower operating costs, improve power usage effectiveness (PUE), and meet sustainability targets, positioning liquid cooling as a strategic solution for energy-intensive, high-density computing environments.

Retrofit Limitations

Retrofitting liquid cooling into existing data centers continues to be challenging due to space constraints, structural limitations, and legacy power and piping layouts. Many older facilities were not designed to accommodate liquid distribution infrastructure, making upgrades costly and complex.

Although modular and containerized liquid-cooled pods are emerging to extend capacity, they often function as incremental solutions rather than full retrofits, limiting scalability within legacy sites.

Operational Risks (Leaks and Reliability)

Operational risks such as coolant leaks and system failures remain a key concern in liquid-cooled data centers. Even with improved sealing and monitoring technologies, any leakage or cooling interruption can lead to equipment downtime, performance degradation, and potential energy losses. These risks make reliability assurance and robust maintenance practices critical for operators considering large-scale deployment.

AI-Driven Infrastructure Expansion

The rapid expansion of AI workloads is creating strong growth opportunities for the data center liquid cooling market. As compute intensity rises, traditional cooling methods struggle to manage heat efficiently, making liquid cooling a preferred solution. Its ability to support high-density racks and maintain performance is positioning it as a standard infrastructure choice for next-generation AI training facilities.

Next-Generation Cooling Technologies

Emerging innovations such as microfluidic cooling are unlocking new efficiency gains in thermal management. Tests by Microsoft show these systems can dissipate heat up to three times more effectively than conventional cold plates. Such breakthroughs are expected to accelerate adoption by improving performance, reliability, and energy efficiency.

|

Segmentations |

List of Sub-Segments |

Segments with High Growth Opportunity |

|

Product-Type Analysis |

Direct-to-chip, Immersion, and Other Products. |

Direct-to-chip holds the largest market share and is projected to experience the fastest growth in the coming years. |

|

Industry-Type Analysis |

Healthcare, Retail, Media & Entertainment, IT & Telecom, BFSI, and Other End-Use Industries. |

IT & Telecom is expected to be the leading category of the market, whereas BFSI is expected to grow at the fastest pace. |

|

Region Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to remain the largest market for data center liquid cooling during the forecast period. |

“Direct-to-chip holds the largest market share and is projected to experience the fastest growth in the coming years.”

The data center liquid cooling market is segmented into direct-to-chip cooling, immersion cooling, and other cooling technologies. Among these, the direct-to-chip segment accounts for the largest market share, dominating nearly three-fourths of the global data center liquid cooling market.

Direct-to-chip liquid cooling systems efficiently transfer heat directly from high-performance processors, significantly reducing energy consumption compared to traditional air cooling solutions. This technology offers easier integration into existing data center infrastructure, making it a preferred choice for hyperscale and enterprise data centers.

For example, NVIDIA has standardized direct-to-chip liquid cooling in its GB200 NVL72 and GB300 NVL72 AI infrastructure systems, which use a closed-loop coolant architecture that avoids evaporation and reduces water usage. The platform is designed to deliver up to 30× higher throughput, 25× greater energy efficiency, and significantly higher compute density compared with traditional air-cooled deployments.

Direct-to-chip solutions today can cool components exceeding 1,600 W, enabling more than 50% higher server density while facility-level energy consumption is reduced by ~40%, reinforcing the segment’s leadership as AI and high-performance computing workloads continue to scale.

Want to get a free sample? Register Here

"Information technology & telecom segment is projected to maintain its position as the largest segment in the market."

The market is segmented into IT & telecom, retail, healthcare, banking, financial services & insurance (BFSI), media & entertainment, and other end-use industries. IT & Telecom is projected to maintain its position as the largest segment in the market, whereas the BFSI sector is anticipated to experience the fastest growth over the forecast period.

The IT & Telecom industry generates high computing demand from AI, machine learning, cloud services, and big data, resulting in significant heat generation that requires liquid cooling. As mobile networks and cloud computing grow, the number of data centers and their cooling needs have surged.

BFSI is the fastest-growing segment as banks rapidly digitize, expand private data centers, and handle high-speed analytics, while regulatory and sustainability pressures drive adoption of energy-efficient liquid cooling solutions.

“North America is expected to remain the largest market, and Asia-Pacific is likely to be the fastest-growing market during the forecast period.”

North America is expected to remain the largest market due to its early adoption of advanced technologies and the rapid growth of connected devices. The region accounts for over 40% of the world’s data centers, reinforcing its leadership. Increased investment in direct-to-chip and immersion cooling, alongside expanding 5G and edge deployments, continues to drive demand. In the United States, operators such as EdgePresence and EdgeMicro are scaling edge facilities, while Canada is expanding capacity to meet rising demand and sustainability goals.

Asia-Pacific has experienced steady growth and a rapidly increasing demand for cloud applications driven by social media, gaming, and entertainment. China's large market plays a significant role in this regional growth. Additionally, the rising adoption of AI, machine learning, and the Internet of Things (IoT) across various regional industries has created a need for advanced cooling systems to manage the heat generated by high-performance computing workloads.

The market plays around data center liquid cooling is moderately concentrated, as more than 50 active companies are present in the market, which are operational in different regions. Most of the major competitors operate in various segments, providing special or comprehensive cooling products.

Here is the list of the Top Players (Based on Dominance)

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

The data center liquid cooling market has witnessed a series of strategic alliances, mergers, and acquisitions, reflecting the industry’s rapid growth and focus on energy-efficient, high-performance cooling solutions.

In April 2025, Fujitsu partnered with Supermicro (U.S.) and Nidec (Japan) to enhance data center energy efficiency. The collaboration integrates liquid-cooling monitoring software, high-performance GPU servers, and efficient cooling systems, boosting power usage effectiveness (PUE) without compromising performance.

In February 2025, Asperitas collaborated with Cisco through the Cisco Engineering Alliance, integrating immersion cooling technologies with Cisco UCS. This provides pre-validated, scalable cooling solutions, facilitating high-performance computing adoption from edge data centers to hyperscale facilities..

In October 2024, Schneider Electric acquired a controlling stake in Motivair Corporation, a leading provider of liquid cooling and thermal management solutions for high-performance computing. This acquisition strengthens Schneider Electric’s end-to-end data center liquid cooling offerings, spanning grid-to-chip and chip-to-chiller solutions globally.

In December 2023, Vertiv completed the acquisition of CoolTera, including patents, trademarks, and intellectual property, enhancing its expertise in high-density liquid cooling solutions for modern data centers worldwide.

The data center liquid cooling market has also seen notable product innovations, driving efficiency, performance, and scalability for AI and high-density deployments.

In October 2024, Hewlett Packard Enterprise (HPE) unveiled the industry’s first 100% fanless direct liquid cooling system, designed to reduce energy and operational costs for large-scale AI deployments, cutting power consumption by up to 90% compared to traditional air cooling..

In October 2024, CoolIT Systems launched new AI cooling solutions, including the AHx240 and AHx180 liquid-to-air CDUs, optimized for the NVIDIA Blackwell AI platform, supported by a major expansion of global manufacturing capacity.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market.

The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Service portfolio, New Product Launches, etc.

COVID-19 impact and its recovery curve.

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

|

Market Study Period |

2018-2031 |

|

Base Year |

2024 |

|

Forecast Period |

2025-2031 |

|

Trend Period |

2018-2023 |

|

Number of Tables & Figures |

>100 |

|

Number of Segments Analysed |

3 (Product Type, End-use Industry Type, and Region) |

|

Number of Regions Analysed |

4 (North America, Europe, Asia-Pacific, Rest of the World) |

|

Countries Analysed |

15 (The USA, Canada, Mexico, Germany, France, Italy, The UK, China, Japan, India, Brazil, Saudi Arabia, Rest of Europe, Rest of APAC, and Rest of the World) |

|

Free Customization Offered |

10% |

|

After Sales Support |

Unlimited |

|

Report Presentation |

Complimentary |

|

Market Dataset |

Complimentary |

|

Further Deep Dive & Consulting Services |

10% Discount |

The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The data center liquid cooling market is segmented into the following categories:

Data Center Liquid Cooling Market, by Product Type

Direct-to-chip

Immersion

Other Product Types

Data Center Liquid Cooling Market, by End-Use Industry Type

IT & Telecom

Retail

Healthcare

Banking, Financial Services & Insurance (BFSI)

Media & Entertainment

Other End-Use Industries

Data Center Liquid Cooling Market, by Region

North America (Country Analysis: The USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, The UK, Russia, and Rest of Europe)

Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

Rest of the World (Country Analysis: Brazil, Argentina, and Others)

This strategic assessment report from Stratview Research provides a comprehensive analysis that reflects today’s data center liquid cooling market realities and future market possibilities for the forecast period.

The report segments and analyzes the market in the most detailed manner to provide a panoramic view of the market.

The vital data/information provided in the report can play a crucial role for market participants and investors in identifying the low-hanging fruits available in the market and formulating growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools.

More than 1,000 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data.

We conducted more than 15 detailed primary interviews with market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Detailed profiling of additional market players (up to three players)

SWOT analysis of key players (up to three players)

Competitive Benchmarking

Benchmarking of key players on the following parameters: Service portfolio, geographical reach, regional presence, and strategic alliances

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The report is delivered digitally through our online portal. Buyers receive login credentials from our team to access the report and may update their credentials at any time after the initial login.

Delivery timelines depend on the status of the report:

For the most accurate delivery timeline, please contact us to confirm the current status of the report.

Yes. You may request a complimentary preview of the report through a video conference with our team.

Yes. The scope of the report can be fully customized to align with your specific research objectives and information requirements.

Please contact us at [email protected], and our team will be happy to discuss your requirements and propose a tailored solution.

Yes. Selected sections of the report can be purchased separately based on your requirements. Please contact us at [email protected] to discuss your needs.

Yes, AI can help gather publicly available information, but its outputs are only as reliable as the data it accesses. Stratview Research reports are built using validated data, extensive primary interviews with industry stakeholders, and the expertise of our experienced research team.

Additionally, many critical insights, including market dynamics, competitive intelligence, and industry-specific trends, are not publicly available and therefore cannot be captured through AI alone.

Liquid cooling technology in data centers manages heat from servers and hardware through five key components: coolant solution (with additives for thermal efficiency), pump (circulates coolant), radiator (dissipates heat), water block (transfers heat), and tubes with fittings (transport coolant).

The market was valued at US$1.3 billion in 2024 and is expected to reach US$7.9 billion in 2031.

The data center liquid cooling market is estimated to grow at a CAGR of 23.2% by 2031, driven by rising data center liquid cooling density, increasing thermal efficiency requirements, and rapid advancements in cooling technologies.

North America is set to remain the largest market, driven by early adoption of new technologies, rising connected devices, and increased investment in direct-to-chip and liquid immersion cooling. The growth of 5G networks and edge data centers, with U.S. operators like EdgePresence and EdgeMicro investing, along with Canada's infrastructure expansion, further fuels market growth.

Asia-Pacific has experienced steady growth and a rapidly increasing demand for cloud applications driven by social media, gaming, and entertainment. China's large market plays a significant role in this regional growth. Additionally, the rising adoption of AI, machine learning, and the Internet of Things (IoT) across various industries in the region has created a need for advanced cooling systems to manage the heat generated by high-performance computing workloads.

Johnson Controls, Vertiv Group Corp, CoolIT Systems, Trane Technologies, Stulz GMBH, Airedale By Modine, Carrier, Daikin Industries, Schneider Electric, Danfoss, are the top players in the Data Center Liquid Cooling market.

IT & Telecom is the leading segment in the market. The industry generates high computing demand from AI, machine learning, cloud services, and big data, resulting in significant heat generation that requires liquid cooling. As mobile networks and cloud computing grow, the number of data centers and their cooling needs has surged.

WE ACCEPT