404

+1-313-307-4176

Aircraft Pneumatic Valves Market

Aircraft Pneumatic Valves Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2024-2034

“The global aircraft pneumatic valves market size was US$ 1.0 billion in 2024 and is likely to grow at a decent CAGR of 4.4% in the long run to reach US$ 1.7 billion in 2034.”

Aircraft pneumatic valves are critical components used in managing and regulating the flow of pressurized air or gases within various systems of an aircraft. These valves play a crucial role in controlling pneumatic operations such as air conditioning, engine starting, anti-icing, cabin pressurization, and actuation systems. They are designed to withstand extreme temperature, pressure, and vibration conditions commonly experienced in aerospace environments, ensuring safe and efficient aircraft performance.

The aircraft pneumatic valves market is experiencing notable growth, driven by several key factors. One of the primary market drivers is the rising production and deliveries of commercial and military aircraft to meet growing air travel demand and defense modernization programs. Additionally, the increasing adoption of advanced pneumatic systems in aircraft for weight reduction and system reliability is pushing manufacturers to innovate and expand their valve offerings. The integration of pneumatic systems in emerging platforms such as unmanned aerial vehicles (UAVs) and next-generation helicopters is further enhancing market potential.

Technological advancements in materials, such as the use of lightweight composites and corrosion-resistant alloys like titanium and stainless steel, are improving valve performance and durability, thereby attracting OEMs and maintenance providers. Moreover, the aftermarket segment is witnessing steady growth due to the rising need for maintenance, repair, and overhaul (MRO) activities, especially as the global aircraft fleet continues to expand and age.

As the aerospace industry continues its post-pandemic recovery and transitions toward sustainable and efficient platforms, the demand for high-performance pneumatic valves is expected to rise significantly, offering ample opportunities for manufacturers, suppliers, and service providers across the value chain.

|

Aircraft Pneumatic Valves Market Report Overview |

|

|

Market Size in 2034 |

USD 1.7 Bn |

|

Market Size in 2024 |

USD 1.0 Bn |

|

Market Growth (2024-2034) |

CAGR of 4.4% |

|

Base Year of Study |

2023 |

|

Trend Period |

2018-2022 |

|

Forecast Period |

2024-2034 |

The market is moderately consolidated with the presence of a fair number of players. Most of the major players are diversified and offering several products targeting the aerospace industry. Furthermore, these companies are part of a large group, making them one of the biggest tier players in the aerospace industry.

Here is the list of the Top Players (Based on Dominance)

Parker Hannifin Corporation

Honeywell International Inc.

Liebherr Group

Transdigm Group Inc.

Woodward Inc.

Raytheon Technologies Corporation

Safran S.A.

Eaton Corporation Plc

General Electric Company

Rolls-Royce Holdings plc

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

|

Segmentations |

List of Sub-Segments |

Segments with High-Growth Opportunity |

|

Aircraft-Type Analysis |

Commercial Aircraft, General Aviation, Regional Aircraft, Military Aircraft, Helicopter, and Unmanned Air Vehicle |

Commercial aircraft are expected to hold the major share of the market and are also likely to be the fastest-growing segment during the forecast period. |

|

Application-Type Analysis |

Engine, Landing-Gear, Wheels and Brakes, ECS, Flight Control, and Air Conditioning |

Engine is anticipated to be the dominant as well as the fastest-growing application of the market throughout the forecast period. |

|

Material-Type Analysis |

Stainless Steel, Titanium, and Aluminium |

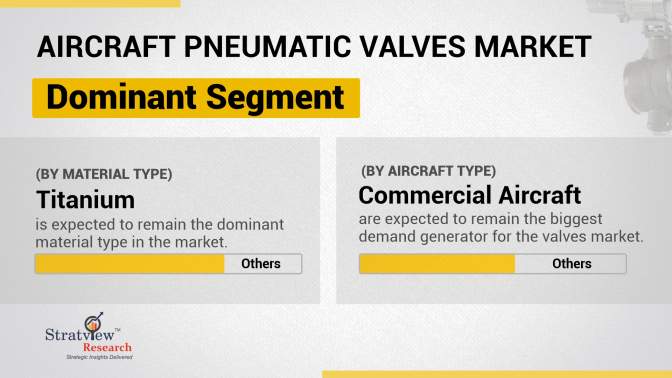

Titanium is projected to hold the largest share and exhibit the fastest growth within the segment. |

|

End-User-Type Analysis |

OEM and Aftermarket |

OEM is expected to remain the dominant end-user type throughout the study period. |

|

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is expected to maintain its reign over the forecast period, whereas Asia-Pacific is likely to grow at the fastest rate. |

“Commercial aircraft are anticipated to be the biggest demand generator of the aircraft pneumatic valves market during the forecast period.”

Based on aircraft type, the market is segmented into commercial aircraft, general aviation, regional aircraft, military aircraft, helicopters, and unmanned air vehicles (UAVs).

Commercial aircraft are anticipated to be the primary demand drivers in the aircraft pneumatic valves market during the forecast period. This dominance is largely attributed to the sustained growth in global air travel and the strong demand for new aircraft deliveries across major airlines. Leading aircraft manufacturers such as Boeing and Airbus project the delivery of approximately 43,975 and 42,430 new commercial aircraft, respectively, over the next two decades, as outlined in their latest market outlooks. This large-scale production pipeline highlights the aerospace industry’s confidence in long-term passenger traffic growth, fleet expansion, and the replacement of older, less efficient aircraft.

This surge in commercial aircraft production directly translates into an increased requirement for high-performance pneumatic systems and associated components, including valves. Pneumatic valves are essential for the operation of various onboard systems such as air conditioning, environmental control systems (ECS), anti-icing, engine start, and flight control systems that are particularly critical in modern commercial jets operating under diverse climatic and operational conditions.

Moreover, the extensive and growing order backlog from major OEMs, estimated at nearly 14,849 aircraft as of early 2025, further reinforces the projected stability and upward trajectory of the commercial aviation segment. These orders not only ensure a steady flow of production but also sustain the aftermarket demand for valve maintenance, replacement, and upgrades. As airlines seek to improve fuel efficiency, reliability, and compliance with evolving environmental regulations, the integration of advanced and lightweight pneumatic valves will remain a top priority, thereby cementing the commercial aircraft segment as the leading contributor to market growth.

“The engine is expected to account for the largest share and register the highest growth within the market throughout the forecast period.”

Based on application type, the market is segmented into engine, landing gears, wheels and brakes, environmental control systems (ECS), flight control, and air conditioning.

Among the various application segments, the engine is expected to dominate the aircraft pneumatic valves market in terms of both market share and growth rate throughout the forecast period. This is primarily due to the critical role pneumatic valves play in several engine-related systems such as engine start, bleed air regulation, anti-icing, and fuel system control. These functions are essential for efficient engine operation, safety, and performance, especially in modern high-bypass turbofan engines used in commercial and military aviation.

As aircraft manufacturers move toward more fuel-efficient and cleaner propulsion technologies, there is an increasing emphasis on optimizing engine systems through the use of advanced pneumatic control components. Pneumatic valves are vital in managing high-temperature and high-pressure air extracted from engines, ensuring proper airflow distribution to other systems such as the ECS and anti-icing systems. As a result, any advancement or increase in engine production, whether for new aircraft platforms or for retrofitting existing fleets, drives demand for next-generation pneumatic valves capable of withstanding extreme conditions.

Moreover, the strong growth outlook for commercial aircraft deliveries, as projected by major OEMs like Boeing and Airbus, indirectly boosts the engine segment’s growth. Each new aircraft requires highly specialized and often custom-engineered valve systems integrated into its propulsion setup. Additionally, the engine segment benefits significantly from the aftermarket, as engines undergo regular inspection, maintenance, and component replacement over their lifecycle. This ensures a sustained demand for replacement pneumatic valves and supports strong growth prospects in the MRO ecosystem.

Want to get a free sample? Register Here

“Titanium is expected to be the most preferred material type in the market during the forecast period.”

Based on material type, the market is segmented into stainless steel, titanium, and aluminium.

Titanium is projected to be the dominant as well as the fastest-growing material type in the aircraft pneumatic valves market during the forecast period. This growing preference is largely due to titanium’s exceptional strength-to-weight ratio, high corrosion resistance, and ability to withstand extreme temperatures and pressures, properties that are critically important for components operating in the harsh conditions of aerospace environments.

As modern aircraft increasingly prioritize fuel efficiency and lightweight design, the aerospace industry is shifting toward advanced materials that reduce overall weight without compromising performance. Titanium’s lightweight nature compared to traditional stainless steel allows aircraft designers to achieve meaningful weight savings, contributing directly to improved fuel efficiency and lower emissions, an increasingly critical factor in the context of stricter environmental regulations and airline cost pressures.

“North America is expected to retain its leading position throughout the forecast period, while Asia-Pacific is projected to witness the fastest growth.”

North America is expected to maintain its dominant position in the aircraft pneumatic valves market throughout the forecast period. This leadership is primarily driven by the presence of major aircraft OEMs, engine manufacturers, and aerospace component suppliers headquartered in the region, including Boeing, Raytheon Technologies, General Electric, and Honeywell Aerospace. These companies account for a significant share of global aircraft production and are at the forefront of developing advanced pneumatic systems. The region also benefits from a robust defense aviation industry, with substantial government investments in military aircraft modernization programs, further supporting demand for high-performance pneumatic valves in both OEM and aftermarket channels.

Additionally, North America's well-established MRO (Maintenance, Repair, and Overhaul) infrastructure contributes to sustained aftermarket demand for pneumatic valve replacements and upgrades. The continued expansion of the commercial aviation industry, coupled with high passenger traffic across the U.S. and Canada, further strengthens the region’s market base. Regulatory emphasis on aircraft safety, performance, and emission standards also drives the adoption of advanced pneumatic technologies in new and existing fleets.

The Asia-Pacific region is projected to witness the fastest growth in the aircraft pneumatic valves market during the forecast period. This rapid expansion is largely fueled by rising air passenger traffic, a growing middle class, and significant investments in indigenous aircraft manufacturing programs across countries like China, India, and Japan. China’s COMAC and India’s HAL are expanding their domestic aerospace capabilities, which is leading to increased demand for local component manufacturing, including pneumatic valves.

Furthermore, several Asia-Pacific airlines have placed large orders for new commercial aircraft to accommodate future travel demand and fleet modernization. The increasing presence of aircraft assembly and component manufacturing facilities in the region, along with supportive government policies and international joint ventures, is accelerating the localization of supply chains. As a result, the Asia-Pacific market is evolving from being a consumption base to a production and innovation hub for aerospace components.

Want to get a free sample? Register Here

This strategic assessment report from Stratview Research provides a comprehensive analysis that reflects today’s aircraft pneumatic valves market realities and future market possibilities for the forecast period. The report segments and analyzes the market in the most detailed manner in order to provide a panoramic view of the market. The vital data/information provided in the report can play a crucial role for market participants and investors in identifying the low-hanging fruit available in the market and formulating growth strategies to expedite their growth process.

This report offers high-quality insights and is the outcome of a detailed research methodology comprising extensive secondary research, rigorous primary interviews with industry stakeholders, and validation and triangulation with Stratview Research’s internal database and statistical tools. More than 500 authenticated secondary sources, such as company annual reports, fact books, press releases, journals, investor presentations, white papers, patents, and articles, have been leveraged to gather the data. We conducted more than 15 detailed primary interviews with market players across the value chain in all four regions and industry experts to obtain both qualitative and quantitative insights.

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

Market structure: Overview, industry life cycle analysis, supply chain analysis.

Market environment analysis: Growth drivers and constraints, Porter’s five forces analysis, SWOT analysis.

Market trend and forecast analysis.

Market segment trend and forecast.

Competitive landscape and dynamics: Market share, Product portfolio, New Product Launches, etc.

COVID-19 impact and its recovery curve

Attractive market segments and associated growth opportunities.

Emerging trends.

Strategic growth opportunities for the existing and new players.

Key success factors.

The aircraft pneumatic valves market is segmented into the following categories:

By Aircraft Type

Commercial Aircraft

General Aviation

Regional Aircraft

Military Aircraft

Helicopter

Unmanned Air Vehicle

By Application Type

Engine

(Valve-Type Analysis: Starter Valve, Bleed Air Valve, Pressure Release Valves, Shut-off Valves, and Other Valves)

(Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

Landing-Gears, Wheels, and Brakes

(Valve-Type Analysis: Brake Control Valve, Dump Valve, and Other Valves)

(Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

ECS

(Valve-Type Analysis: Engine Anti-Icing Valve, Wing Anti-Icing Valve, Pressure Reducing Valve, and Other Valves)

(Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

Flight Control

(Valve-Type Analysis: Shuttle Valve, Check Valve, and Other Valves)

(Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

Air Conditioning

(Valve-Type Analysis: Pack Valve, Isolating Valve, Cross-Bleed Valve, and Other Valves)

(Regional Analysis: North America, Europe, Asia-Pacific, and Rest of the World)

By Material Type

Stainless Steel

Titanium

Aluminium

By End-User Type

OEM

Aftermarket

By Region

North America (Country Analysis: The USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, The UK, Russia, and the Rest of Europe)

Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others)

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Detailed profiling of additional market players (up to three players)

SWOT analysis of key players (up to three players)

Competitive Benchmarking

Benchmarking of key players on the following parameters: Service portfolio, geographical reach, regional presence, and strategic alliances

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

A considerable number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

In June 2025, Crane Co., a Stamford-based industrial manufacturer, announced a US$1.15 billion cash acquisition of Baker Hughes’ Precision Sensors & Instrumentation (PSI) unit, which includes brands like Druck, Panametrics, and Reuter‑Stokes.

In September 2022, Parker Hannifin finalized its US$8.2 billion acquisition of Meggitt. Meggitt is an international group and a world leader in the aerospace, defence, and energy markets.

An aircraft pneumatic valve is a specialized component used to control the flow, direction, and pressure of compressed air within an aircraft's pneumatic system. These valves play a critical role in various onboard functions such as cabin pressurization, environmental control, de-icing, door actuation, and braking systems. Designed to operate reliably under extreme conditions, pneumatic valves ensure precise air management and are often integrated with electronic controls for improved automation and performance in both commercial and military aircraft.

The aircraft pneumatic valves market is projected to expand at a compound annual growth rate (CAGR) of 4.4% in the coming years, with its total value expected to reach approximately US$ 1.7 billion by 2034.

The aircraft pneumatic valves market is primarily driven by the growing global aircraft fleet and the rising production rates of commercial and military aircraft to meet increasing air travel and defense demands. Technological advancements in pneumatic systems that offer higher efficiency, reduced weight, and improved reliability are encouraging their adoption across next-generation aircraft platforms. Additionally, the expanding MRO (Maintenance, Repair, and Overhaul) industry is fueling aftermarket demand for valve replacements and upgrades. Regulatory emphasis on safety, performance, and environmental compliance is also prompting the use of advanced materials and precision-engineered valve solutions, further propelling market growth.

North America represents the largest segment of the aircraft pneumatic valves market, primarily due to the strong presence of leading aerospace manufacturers such as Boeing, Lockheed Martin, and Raytheon Technologies. The region benefits from well-established aviation infrastructure, ongoing investments in military and commercial aircraft programs, and a high demand for advanced aircraft systems. Additionally, the U.S. Department of Defense’s focus on modernizing air fleets and the steady recovery of the commercial aviation industry further contribute to North America’s dominant position in the market.

Asia-Pacific is the fastest-growing region in the aircraft pneumatic valves market, driven by rising air travel demand, rapid fleet expansion, and increasing investments in domestic aircraft manufacturing programs. Countries like China, India, and Japan are significantly boosting their aerospace capabilities through both government-led initiatives and private industry participation. The emergence of regional aircraft manufacturers such as COMAC and HAL, coupled with infrastructure development and growing MRO (Maintenance, Repair, and Overhaul) activities, is accelerating the adoption of advanced pneumatic systems across the region.

Parker Hannifin Corporation, Honeywell International Inc., Liebherr Group, Transdigm Group Inc., Woodward Inc., Raytheon Technologies Corporation, Safran S.A., Eaton Corporation Plc, and General Electric Company are the leading players in the aircraft pneumatic valves market.

The engine segment holds the dominant position in the aircraft pneumatic valves market by application type. This is due to the critical role pneumatic valves play in engine-related functions such as bleed air management, engine start, anti-icing, and fuel control. As modern aircraft engines become more advanced and operate under extreme pressure and temperature conditions, the demand for high-performance pneumatic valves continues to grow. Additionally, the increasing production of commercial and military aircraft, along with the steady growth of the aftermarket for engine maintenance and upgrades, reinforces the engine segment’s leading status in the market.

WE ACCEPT