404

+1-313-307-4176

Aerospace Pressure Bulkhead Market Analysis | 2026-2034

Aerospace Pressure Bulkhead Market Size, Share, Trend, Forecast, Competitive Analysis, and Growth Opportunity: 2026-2034

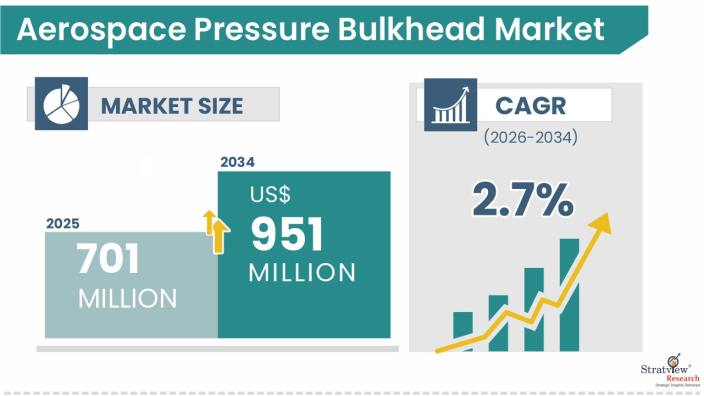

“The aerospace pressure bulkhead market size was USD 701 million in 2025 and is likely to grow at a decent CAGR of 2.7% during 2026-2034 to reach USD 951 million in 2034.”

Want to know more about the market scope? Register Here

Aerospace pressure bulkheads are essential structural barriers built into aircraft fuselages that separate the pressurized passenger cabin from unpressurized sections like the tail cone, cargo areas, and equipment bays. These components face demanding conditions during every flight, managing pressure differences of around 8 to 9 psi between the cabin and outside atmosphere while enduring repetitive stress cycles over thousands of flights. The rear pressure bulkhead, particularly in narrow-body and wide-body jets, typically takes on a curved, dome-like shape, a design choice that effectively spreads out the enormous forces acting on it. These bulkheads do more than just hold pressure; they reinforce the overall airframe structure, provide attachment points for critical flight control components, and in some cases act as protective fire barriers.

The aerospace pressure bulkhead market represents a specialized niche within aircraft manufacturing, closely tied to the fortunes of commercial aviation production and military aircraft programs. Market growth tracks directly with aircraft delivery schedules from major manufacturers like Airbus, Boeing, and COMAC, alongside the substantial aftermarket driven by airlines replacing bulkheads in older aircraft showing fatigue damage. The industry is currently navigating a significant materials shift, moving from traditional aluminum alloys toward advanced options including aluminum-lithium variants, carbon fiber composites, and innovative hybrid constructions that promise weight savings without compromising safety. Manufacturing remains concentrated in North America and Europe where aerospace expertise runs deep, though Asia-Pacific is rapidly building capabilities through domestic aircraft programs and expanding maintenance operations. The market's character is shaped by lengthy certification timelines that can span years, ongoing consolidation among major suppliers, and the technical complexities of fitting pressure bulkheads into the composite fuselage designs that define modern aircraft architecture.

A moderate number of strategic alliances, including M&As, JVs, etc., have been performed over the past few years:

|

Segmentations |

List of Sub-Segments |

Dominant and Fastest-Growing Segments |

|

Aircraft-Type Analysis |

Narrow-Body Aircraft, Wide-Body Aircraft, Regional Aircraft, and General Aviation |

Narrow-Body aircraft is projected to remain the dominant aircraft type throughout the forecast period. |

|

Material-Type Analysis |

Metal Pressure Bulkhead and Composite Pressure Bulkhead |

Composite pressure bulkheads are forecasted to grow at the fastest rate among all the material types. |

|

Shape-Type Analysis |

Flat Pressure Bulkhead and Curved Pressure Bulkhead |

Flat pressure bulkhead is expected to remain the leading shape for aerospace pressure bulkhead throughout the forecast period. |

|

Manufacturing Process-Type Analysis |

Sheet Stamping, Resin Infusion, and Prepreg |

Resin infusion is expected to be the fastest-growing manufacturing process throughout the forecast period. |

|

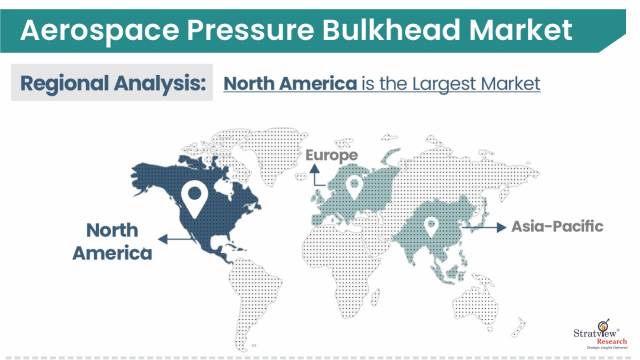

Regional Analysis |

North America, Europe, Asia-Pacific, and The Rest of the World |

North America is likely to retain its position as the dominant market for the aerospace pressure bulkhead till 2034. |

“Narrow-body aircraft are projected to remain the dominant aircraft type, while wide-body aircraft are expected to register the fastest growth during the forecast period.”

The aerospace pressure bulkhead market is segmented by aircraft-type into narrow-body aircraft, wide-body aircraft, regional aircraft, and general aviation.

Narrow-body aircraft is expected to maintain its dominant position in the aerospace pressure bulkhead market due to fundamentally higher production volumes and fleet sizes compared to other aircraft categories. Single-aisle aircraft such as the Boeing 737 MAX family and Airbus A320neo series represent the backbone of global commercial aviation, with manufacturers maintaining monthly production rates that significantly exceed wide-body output. Each narrow-body aircraft requires multiple pressure bulkheads, typically including forward and aft bulkheads plus additional bulkheads separating pressurized cargo holds, creating substantial per-unit demand. Additionally, the aftermarket replacement cycle for narrow-body pressure bulkheads remains robust, as these aircraft accumulate flight cycles more rapidly than wide-bodies, accelerating fatigue-related component degradation. Low-cost carriers expanding across Asia-Pacific, Middle East, and Latin America further amplify narrow-body demand, with multiple operators maintaining order books stretching years into the future.

Wide-body aircraft is projected to experience the fastest growth in the market, driven by several converging factors in the current global air transport landscape. The emergence of ultra-long-haul routes, exemplified by Singapore Airlines' non-stop services exceeding 18 hours and Qantas's Project Sunrise initiatives targeting direct flights from Australia to New York and London, is pushing demand for next-generation wide-bodies with advanced structural designs capable of extended operations. Airlines are accelerating replacement of aging Boeing 777 classics and early A330 variants with fuel-efficient platforms like the 787 Dreamliner, A350 XWB, and incoming 777-9, which feature larger, more structurally sophisticated pressure bulkheads engineered for greater cabin volumes and extended operational lifespans. The shift toward composite-intensive wide-body construction presents growth opportunities, as manufacturers like Boeing with 50% composite content on the 787 and Airbus with 53% on the A350 require advanced composite pressure bulkheads that integrate seamlessly with carbon fiber fuselage barrels, a departure from traditional aluminum designs.

“Metal pressure bulkheads are expected to continue leading the market by material type, whereas composite pressure bulkheads are projected to experience the highest growth rate over the forecast period.”

The market is segmented by material type into metal pressure bulkhead, and composite pressure bulkhead.

Metal pressure bulkheads retain their market-leading position due to their proven reliability across decades of commercial aviation service and continued dominance in existing aircraft platforms. Aluminum alloys, particularly the 2000 and 7000 series variants, remain the material of choice for most in-production narrow-body aircraft including the Boeing 737 MAX and significant portions of the A320neo family, benefiting from well-established manufacturing processes, predictable material behavior, and extensive certification databases that streamline regulatory approval. The global fleet of legacy aircraft representing thousands of B737NGs, A320neos, B767s, and older wide-bodies, exclusively utilize metal pressure bulkheads, generating sustained aftermarket demand for replacement components as these aircraft approach their mid-life and end-of-life service intervals.

Composite pressure bulkheads are likely to experience the highest growth throughout the forecast period as aerospace manufacturers pursue aggressive weight reduction targets and design next-generation aircraft around carbon fiber reinforced polymer (CFRP) airframes. The Boeing 787 and Airbus A350 have demonstrated that composite pressure bulkheads can meet stringent airworthiness requirements while delivering weight savings of 20-25% compared to equivalent metal designs, translating directly to fuel efficiency gains and increased payload capacity over an aircraft's operational lifetime. New aircraft programs entering development including potential future narrow-body replacements and advanced regional jets, are being designed from the outset with composite-intensive structures, necessitating pressure bulkheads that integrate seamlessly with CFRP fuselage sections to avoid problematic material interfaces and galvanic corrosion issues that arise in hybrid metal-composite joints.

“Flat pressure bulkheads are expected to remain the more widely adopted shape, while curved pressure bulkheads are projected to grow at the highest rate over the forecast period.”

The market is segmented into flat pressure bulkhead and curved pressure bulkhead.

Flat pressure bulkheads are likely to maintain their dominance due to their extensive application across multiple aircraft zones and inherent manufacturing advantages. These planar structures are the standard choice for forward pressure bulkheads separating the cockpit from unpressurized nose sections, bulkheads dividing pressurized and unpressurized cargo compartments in narrow-body aircraft, and partition bulkheads within cabin sections that don't experience full differential pressure loads. The manufacturing economics strongly favor flat designs, as they can be fabricated using conventional sheet metal forming, machining, and layup processes without requiring complex tooling for compound curvatures, reducing both production costs and lead times compared to curved alternatives. Quality control and inspection procedures for flat bulkheads are more straightforward, allowing technicians to easily verify dimensional tolerances, detect manufacturing defects, and perform non-destructive testing across the entire surface area without specialized access equipment. The repair and replacement advantages of flat bulkheads further reinforce their market dominance, as maintenance crews can access these components more easily during scheduled inspections and execute repairs using standard practices that don't require the specialized fixtures needed for curved bulkhead work.

Curved pressure bulkheads are expected to experience a higher growth rate driven by their superior structural efficiency in handling primary cabin pressurization loads and increasing adoption in modern aircraft designs. The hemispherical or dome-shaped aft pressure bulkhead, which bears the full cabin-to-ambient pressure differential in most commercial aircraft, demonstrates why curved geometry dominates this critical application, the spherical shape distributes stress uniformly across the structure, minimizing peak stress concentrations and allowing thinner, lighter designs compared to equivalent flat bulkheads that would require substantial reinforcement to resist the same loads. Wide-body aircraft expansion directly amplifies curved bulkhead demand, as larger fuselage diameters create proportionally greater pressure loads that make curved designs not just advantageous but structurally necessary. The aerospace industry's evolving understanding of damage tolerance is favoring curved composite bulkheads, as finite element analysis and full-scale testing have demonstrated that properly designed curved CFRP structures exhibit excellent crack propagation resistance and fail-safe characteristics when engineered with appropriate ply layups and thickness variations, this further supports the growing demand for curved pressure bulkheads.

“Sheet stamping is forecasted to maintain its position as the primary manufacturing method, whereas resin infusion is expected to grow at the most rapid pace over the forecast period.”

The market is segmented into sheet stamping, resin infusion, and prepreg.

Sheet stamping is expected to retain its lead due to its proven capability to efficiently produce metal components at the production volumes demanded by narrow-body aircraft programs. This well-established process uses high-tonnage hydraulic or mechanical presses with precision dies to form aluminum alloy sheets into the required bulkhead geometry in a single operation or through progressive forming stages, achieving the tight dimensional tolerances necessary for aircraft assembly while maintaining excellent repeatability across thousands of units. The process dominates flat pressure bulkhead production for forward and cargo compartment applications in single-aisle jets, where relatively simple geometries and aluminum construction align perfectly with its capabilities. North American suppliers, concentrated around Boeing facilities in Washington and Spirit AeroSystems operations in Kansas, have refined sheet stamping techniques over decades, while European manufacturers supporting Airbus production have developed parallel capabilities. This regional manufacturing expertise creates significant barriers to rapid process substitution.

Resin infusion is likely to be the fastest-growing manufacturing process, especially as composite pressure bulkheads are becoming more popular in both narrow-body and wide-body aircraft programs. Manufacturers are on the lookout for ways to enhance material properties while keeping production costs in check. This method, which includes techniques like vacuum-assisted resin-transfer molding (VARTM) and resin film infusion (RFI), involves placing dry carbon fiber preforms onto molds and then introducing liquid resin under controlled vacuum or pressure. This results in composite parts with fiber-to-resin ratios of 55-60%, effectively eliminating voids and porosity issues that can weaken structural integrity in traditional hand layup methods. The impressive mechanical properties gained through resin infusion are especially crucial for the curved composite pressure bulkheads found in wide-body aircraft like the 787 and A350. These hemispherical aft bulkheads need to endure significant pressure loads while fitting perfectly with the surrounding carbon fiber fuselage barrels. With resin infusion, manufacturers can ensure consistent material quality throughout the thickness of the component, which is vital for meeting damage tolerance standards over more than 50,000 flight cycles.

“North America is likely to remain the leading market for aerospace pressure bulkheads, whereas Asia-Pacific is projected to experience the fastest growth during the forecast period.”

North America is likely to maintain its position as the leading market for aerospace pressure bulkheads, anchored by the region's unparalleled concentration of major aircraft manufacturers, tier-1 aerostructures suppliers, and decades of accumulated aerospace engineering expertise. Boeing's commercial aircraft production facilities in Washington state and South Carolina create a huge demand for pressure bulkheads across the 737 MAX, 767, 777, and 787 programs. Also, with Boeing's acquisition of Spirit AeroSystems in December 2025 bringing Spirit's operations in Wichita, Dallas, and Tulsa under its wing critical bulkhead manufacturing capabilities have become even more centralized within North America. The local supplier ecosystem is filled with specialized manufacturers who excel in both metal and composite pressure bulkhead production. Their proximity to major OEM final assembly lines allows for just-in-time delivery and fosters collaborative engineering relationships, which are vital for navigating the complex design changes that come with multi-year aircraft development programs.

On the other hand, the Asia-Pacific region is set to experience the fastest growth due to an incredible surge in commercial aviation and a surge in local aircraft manufacturing efforts. According to the latest Airbus and Boeing forecasts, China is expected to require over 9,000 new aircraft over the next two decades, this massive fleet expansion will create a significant need for pressure bulkheads, particularly for narrow-body aircraft that operate on busy domestic routes, as well as for wide-body aircraft that are essential for developing long-haul international networks. The region's growth is fueled by a rise in air travel, an increase in airline fleets, and ongoing defense modernization initiatives, all of which are driving up the demand for pressure bulkheads. On top of that, government policies aimed at boosting aerospace manufacturing and technology development are paving the way for new supply chains and partnerships with international players, solidifying Asia-Pacific's position as the fastest-growing market in the global aerospace pressure bulkhead industry.

Know the high-growth countries in this report. Register Here

The market is moderately consolidated, with the top five players accounting for a significant share of total revenue. Leading companies compete primarily on advanced composite and metallic structure integration capabilities, expertise in designing lightweight yet high-strength bulkhead architectures, and the ability to meet stringent airworthiness and damage-tolerance requirements. The following are the key players in the aerospace pressure bulkhead market:

Note: The above list does not necessarily include all the top players in the market.

Are you the leading player in this market? We would love to include your name. Please write to us at [email protected]

This report provides market intelligence most comprehensively. The report structure has been kept so that it offers maximum business value. It provides critical insights into market dynamics and will enable strategic decision-making for existing market players as well as those willing to enter the market. The following are the key features of the report:

This report studies the market, covering a period of 12 years of trends and forecasts. The report provides detailed insights into the market dynamics to enable informed business decision-making and growth strategy formulation based on the opportunities present in the market.

The aerospace pressure bulkhead market is segmented into the following categories.

Aerospace Pressure Bulkhead Market, by Aircraft Type

Aerospace Pressure Bulkhead Market, by Material Type

Aerospace Pressure Bulkhead Market, by Shape Type

Aerospace Pressure Bulkhead Market, by Manufacturing Process Type

Aerospace Pressure Bulkhead Market, by Region

With this detailed report, Stratview Research offers one of the following free customization options to our respected clients:

Company Profiling

Competitive Benchmarking

Custom Research: Stratview Research offers custom research services across industries. In case of any custom research requirement related to market assessment, competitive benchmarking, sourcing and procurement, target screening, and others, please send your inquiry to [email protected]

The aerospace pressure bulkhead market is estimated to grow at a CAGR of 2.7% by 2034, supported by increasing commercial aircraft production, fleet modernization programs, and rising use of composite fuselage structures. Demand is further driven by weight-reduction initiatives, higher cabin pressurization performance requirements, and the transition toward advanced manufacturing processes such as resin infusion and automated fiber placement.

The forecasted value of the aerospace pressure bulkhead market is expected to be USD 951 million in 2034.

Aernnova Aerospace, Airbus Group, AVIC SAC Commercial Aircraft Company Ltd, Kawasaki Heavy Industries, Mubea Group, PFW Aerospace, Qarbon Aerospace, and Spirit AeroSystems are the leading players in the market.

North America is estimated to remain dominant in the market in the foreseeable future due to the tpresence of major aircraft OEMs, established aerostructures suppliers, and high production volumes of both narrow-body and wide-body aircraft. Strong defense aviation programs and early adoption of advanced composite fuselage technologies further reinforce regional leadership.

Asia-Pacific is estimated to remain the fastest-growing market for aerospace pressure bulkhead in the foreseeable future, driven by rapid airline fleet expansion, indigenous aircraft programs in China, India, and Japan, and increasing localization of aerostructures manufacturing supported by government industrial policies.

Metal pressure bulkheads are expected to remain dominant due to their proven structural reliability, fatigue resistance, and cost efficiency.

WE ACCEPT